Martes, 28 de julio de 2026

Get Ready: EU budgetary austerity is back

NICOLÁS AZNAREZ

If you follow EU issues you may have probably heard about the recent note prepared by the Spanish presidency of the Council proposing cuts to the EU’s long-term budget for 2021-2027. This may sound strange. Isn’t the next European Council supposed to discuss the Commission’s so-called “MFF mid-term revision” , a proposal to increase the EU budget?

Against this background, the Commission proposes an increase by €66 bn the EU spending for 2024-2027. Roughly a quarter of this increase (€17bn) is to finance a new “Ukraine facility” providing support to Ukraine during the next four years (coupled with loans which are not 'paid' but guaranteed by the EU budget). Another quarter is to cover the higher-than-expected borrowing costs of Next Generation Union (€19bn). The rest is to reinforce migration and external action (€15.5 bin) and to finance the Strategic Technologies for Europe Platform (STEP), a new EU instrument to support investments in critical technologies relevant to Union’s strategic autonomy (€10bn).

Since the announcement in June, the so-called ‘frugal countries’ (Germany, Sweden, Denmark, Austria and the Netherlands) have made clear their opposition to any EU spending increase other than to support Ukraine. Over the last months, they have circulated internal notes showing that new EU spending needs can be covered through re-deployments, e.g. cutting EU spending elsewhere. Recent events (the victory of Geert Wilders in the Netherlands, the massive budgetary hole in Germany following the decision of the Constitutional Court of November 15) do nothing more than reinforcing the frugals’ opposition against any reinforcement of the EU budget.

This is why the Spanish presidency of the Council, as a good ‘broker’, has come up with a proposal of budgetary ‘savings’. An internal note sent to the national delegations ketches three scenarios of cuts. Each scenario results from applying a different % of linear cuts to all MFF programs except the CAP and Cohesion programs ( 3.4%, 6,8% and 13.5%), which are fiercely defended by net recipient countries. They also include reductions to certain programs that have been largely unused (such as the Brexit Adjustment Reserve). The three scenarios result into cuts of €8.1bn, €13.1bn and €23.1bn respectively.

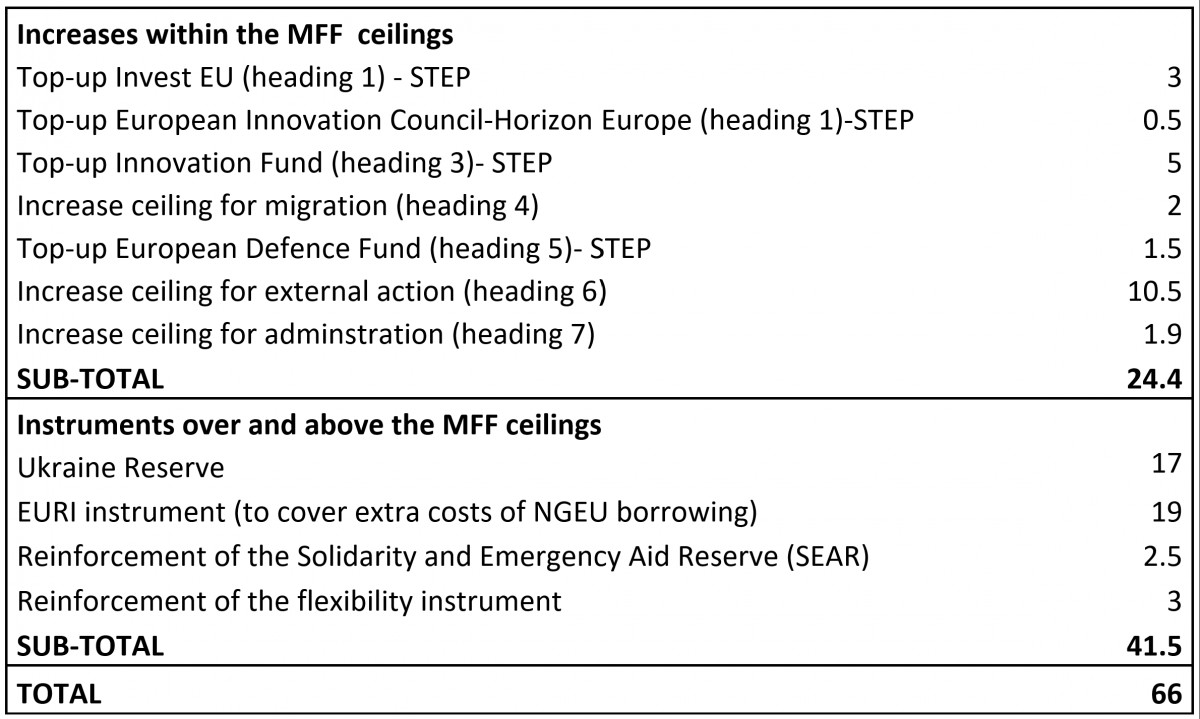

But why the most ambitious scenario amounts to €23.1bn in savings and not €49bn? (which would be the result from discounting the €17bn for Ukraine from the total €66bn)? A detailed look at the proposals included in the Commission’s mid-term revision may provide an answer (see Table 1).

Se puede leer el artículo en español

[Recibe los análisis de más actualidad en tu correo electrónico o en tu teléfono a través de nuestro canal de Telegram]

To understand what is happening, it is worth going back to June, when the Commission presented the “mid-term revision” proposal. This was motivated by the awareness that the EU budget cannot provide an appropriate answer to various challenges which were unpredictable in December 2020, when the current EU’s long-term budget was adopted. This includes the war in Ukraine and the unfolding humanitarian, energy and food crises but also other things such as the steep increase of interest rates in international markets, which has led to higher-than-expected NGEU borrowing costs, or the adoption of the US Inflation Reduction Act, a massive US investment package in support of green technologies. Against this background, the Commission proposes an increase by €66 bn the EU spending for 2024-2027. Roughly a quarter of this increase (€17bn) is to finance a new “Ukraine facility” providing support to Ukraine during the next four years (coupled with loans which are not 'paid' but guaranteed by the EU budget). Another quarter is to cover the higher-than-expected borrowing costs of Next Generation Union (€19bn). The rest is to reinforce migration and external action (€15.5 bin) and to finance the Strategic Technologies for Europe Platform (STEP), a new EU instrument to support investments in critical technologies relevant to Union’s strategic autonomy (€10bn).

Since the announcement in June, the so-called ‘frugal countries’ (Germany, Sweden, Denmark, Austria and the Netherlands) have made clear their opposition to any EU spending increase other than to support Ukraine. Over the last months, they have circulated internal notes showing that new EU spending needs can be covered through re-deployments, e.g. cutting EU spending elsewhere. Recent events (the victory of Geert Wilders in the Netherlands, the massive budgetary hole in Germany following the decision of the Constitutional Court of November 15) do nothing more than reinforcing the frugals’ opposition against any reinforcement of the EU budget.

This is why the Spanish presidency of the Council, as a good ‘broker’, has come up with a proposal of budgetary ‘savings’. An internal note sent to the national delegations ketches three scenarios of cuts. Each scenario results from applying a different % of linear cuts to all MFF programs except the CAP and Cohesion programs ( 3.4%, 6,8% and 13.5%), which are fiercely defended by net recipient countries. They also include reductions to certain programs that have been largely unused (such as the Brexit Adjustment Reserve). The three scenarios result into cuts of €8.1bn, €13.1bn and €23.1bn respectively.

But why the most ambitious scenario amounts to €23.1bn in savings and not €49bn? (which would be the result from discounting the €17bn for Ukraine from the total €66bn)? A detailed look at the proposals included in the Commission’s mid-term revision may provide an answer (see Table 1).

Table 1. Different spending increases proposed in the MFF mid-term revision

There are two types of spending proposals in the MFF mid-term revision: top-ups to existing MFF programs and reinforcements and/or creation of special instruments which are placed over and above’ the MFF ceilings. These two spending proposals have very different implications for national finance ministers. The first ones result into clear, measurable and immediate budgetary costs for national coffers. The second ones will be mobilised according to future needs which can be roughly estimated but not known in advance.

Take the case of the Ukraine facility. The annual amount disbursed in support to Ukraine will depend on the Ukraine government's progress in implementing a Reconstruction Plan. The same happens with the proposed EURI instrument, aimed at covering the NGEU borrowing costs in excess of those planned (and reserved) in the MFF. These could range from €17bn to €27bn according to Commission's estimations but we cannot know in advance, it will depend on interest rate fluctuations.

Thus, the logic of the proposed cuts is to force redeployments within the MFF ceilings. In the case of STEP, for instance, the Commission proposes to finance it with additional €10bn and a minor amount (€2.13bn) coming from redeployments. It is very likely that the Council decides to entirely finance it through re-deployments and re-using decommitment amounts from Horizon Europe.

This does not mean that the proposals to create new instruments “over and above the MFF” are guaranteed. As we are heading towards the December European Council, a stubborn Hungary is still threating to block all EU's aid to Ukraine and some 'frugals' flirt with the idea of covering the NGEU extra borrowing costs through redeployments from existing MFF programs.

All in all, one may argue it´s classic, old EU budget politics at play: frugals pushing for cuts, net beneficiaries fighting to keep cohesion/CAP funds and non-allocated EU spending being sacrificed. However, after NGEU, two major crises behind us and a new geopolitical context forcing the EU to take a more strategic turn, it is very worrying to see that we may be entering into a new era of EU budgetary austerity.

Take the case of the Ukraine facility. The annual amount disbursed in support to Ukraine will depend on the Ukraine government's progress in implementing a Reconstruction Plan. The same happens with the proposed EURI instrument, aimed at covering the NGEU borrowing costs in excess of those planned (and reserved) in the MFF. These could range from €17bn to €27bn according to Commission's estimations but we cannot know in advance, it will depend on interest rate fluctuations.

Thus, the logic of the proposed cuts is to force redeployments within the MFF ceilings. In the case of STEP, for instance, the Commission proposes to finance it with additional €10bn and a minor amount (€2.13bn) coming from redeployments. It is very likely that the Council decides to entirely finance it through re-deployments and re-using decommitment amounts from Horizon Europe.

This does not mean that the proposals to create new instruments “over and above the MFF” are guaranteed. As we are heading towards the December European Council, a stubborn Hungary is still threating to block all EU's aid to Ukraine and some 'frugals' flirt with the idea of covering the NGEU extra borrowing costs through redeployments from existing MFF programs.

All in all, one may argue it´s classic, old EU budget politics at play: frugals pushing for cuts, net beneficiaries fighting to keep cohesion/CAP funds and non-allocated EU spending being sacrificed. However, after NGEU, two major crises behind us and a new geopolitical context forcing the EU to take a more strategic turn, it is very worrying to see that we may be entering into a new era of EU budgetary austerity.

Se puede leer el artículo en español

ARTÍCULOS RELACIONADOS

Eulalia Rubio

Investigadora principal sobre asuntos económicos europeos en el Instituto Jacques Delors

Es investigadora principal sobre asuntos económicos europeos. Sus principales campos de especialización son el presupuesto de la UE, la elaboración de la política presupuestaria de la UE y las políticas y estrategias europeas de inversión pública. Es autora de numerosos artículos e informes políticos sobre estos temas, incluidos varios informes para el Parlamento Europeo. En los últimos años ha trabajado en particular sobre el Plan de Recuperación de Covid de la UE, el papel del BEI y de los bancos nacionales de desarrollo en apoyo de las políticas de la UE, la dimensión financiera del acuerdo ecológico de la UE y el componente de inversión de la estrategia industrial de la UE.

Es Doctora en Ciencias Políticas por el Instituto Universitario Europeo (Florencia) y Master en Políticas Públicas y Sociales por la Universidad Pompeu Fabra (UPF). Antes de incorporarse al IDJ fue profesora asociada de política comparada en la Universidad Pompeu Fabra (Barcelona) y ayudante de investigación y docencia en el Departamento de Ciencias Políticas y Sociales de la Universidad Pompeu Fabra (UPF). Desde 2014 hasta 2017 también fue profesora asociada sobre gobernanza económica europea en la Escuela Europea de Ciencias Políticas y Sociales (ESPOL).

Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 159 semanas

France, the European Commission, and the Bloody Long Term: Adapt or miss the train

Hace 160 semanas

Germany in Recession: What are the causes, and what does it mean for the European Union?

Lo más leído