Martes, 28 de julio de 2026

France, the European Commission, and the Bloody Long Term: Adapt or miss the train

CHRISTOPHE PETIT TESSON (EFE)

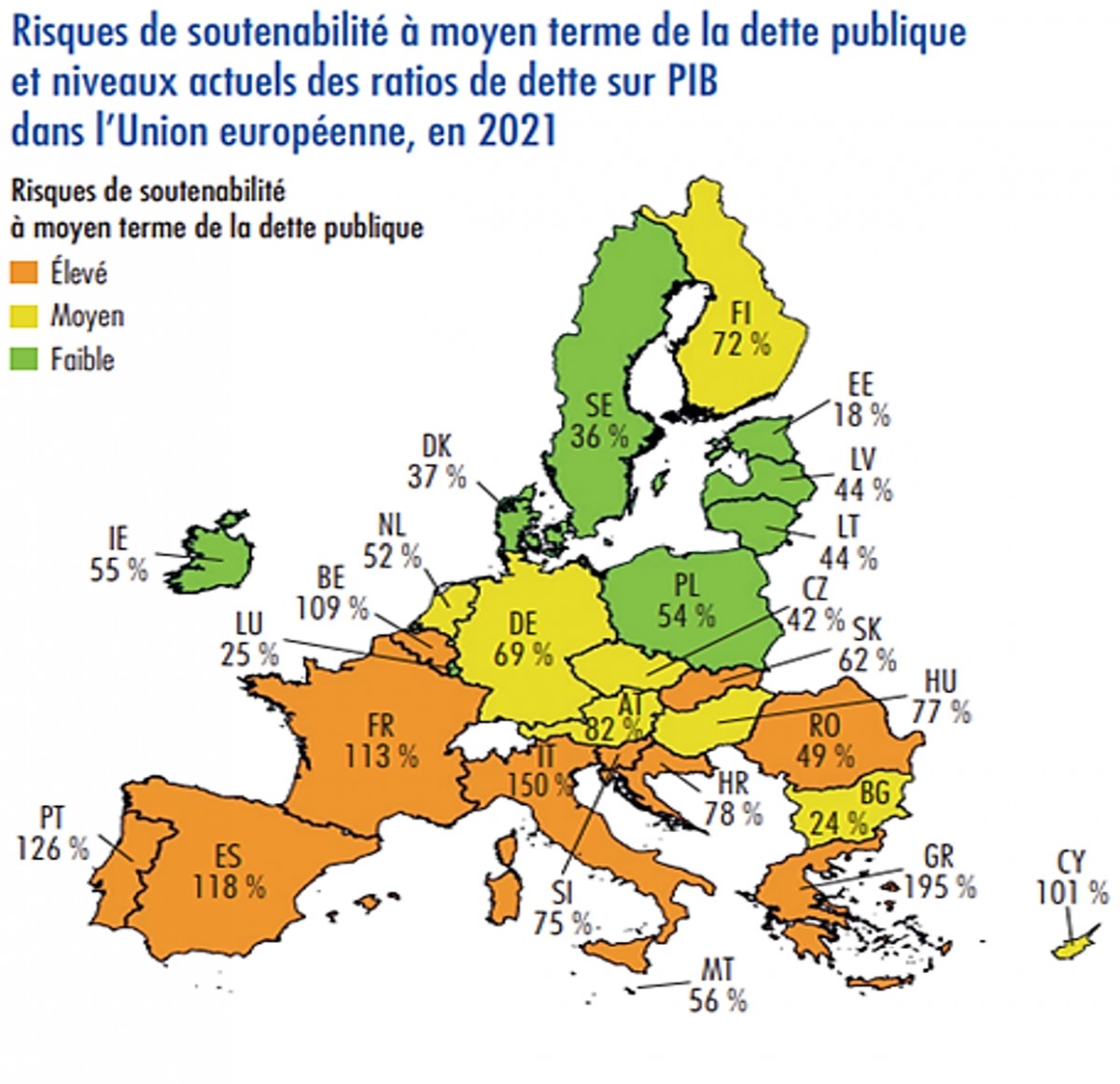

On 19 June in Bercy, Paris, the French Minister of Economy and Finance, Bruno Le Maire, outlined the national budget plan for the coming year 2024 during the public finance workdays (Les Assises). In an event that brought together social partners, representatives of the nation’s various institutional bodies and Prime Minister Élisabeth Borne, the various objectives to be tackled in the coming years were set out. And while it may seem that in principle the plan is simply to stabilise the economy in the run-up to the crucial election in 2027 -which although so far away is no less important-, the truth is that the plan is actually related to the long-term national economic and productive strategy: namely, the government is committed to budgetary stability and sound national accounts with a view to the challenges of the 2030-50 decades. This implies making efforts to reduce the Debt/GDP ratio, which currently stands at around 110% and is one of the highest in the Eurozone (with the permission of Spain, Italy, and Portugal, among others), as can be seen in the figure below. Although the data are for the year 2021, the levels have not changed much in the case of France.

• Return to the 3% public deficit track.

• Bring the debt down from 111.6% to 108.3% by 2027.

• Phasing out the expansionary packages put in place to alleviate the effects of COVID-19 and the energy market crisis in 2022.

• A reduction in public spending that does not involve raising taxes on households, with the intention of not affecting household purchasing power.

The statements by Le Maire and Borne send a message to Brussels and their European colleagues: the commitment to the new EU fiscal governance rules is clear. Everything indicates, therefore, that the government intends to fly the flag of responsible management in the face of the effervescence of the political left and the aggressiveness of the Rassemblement National, which is the real opposition in parliament and the rival to beat in 2027.

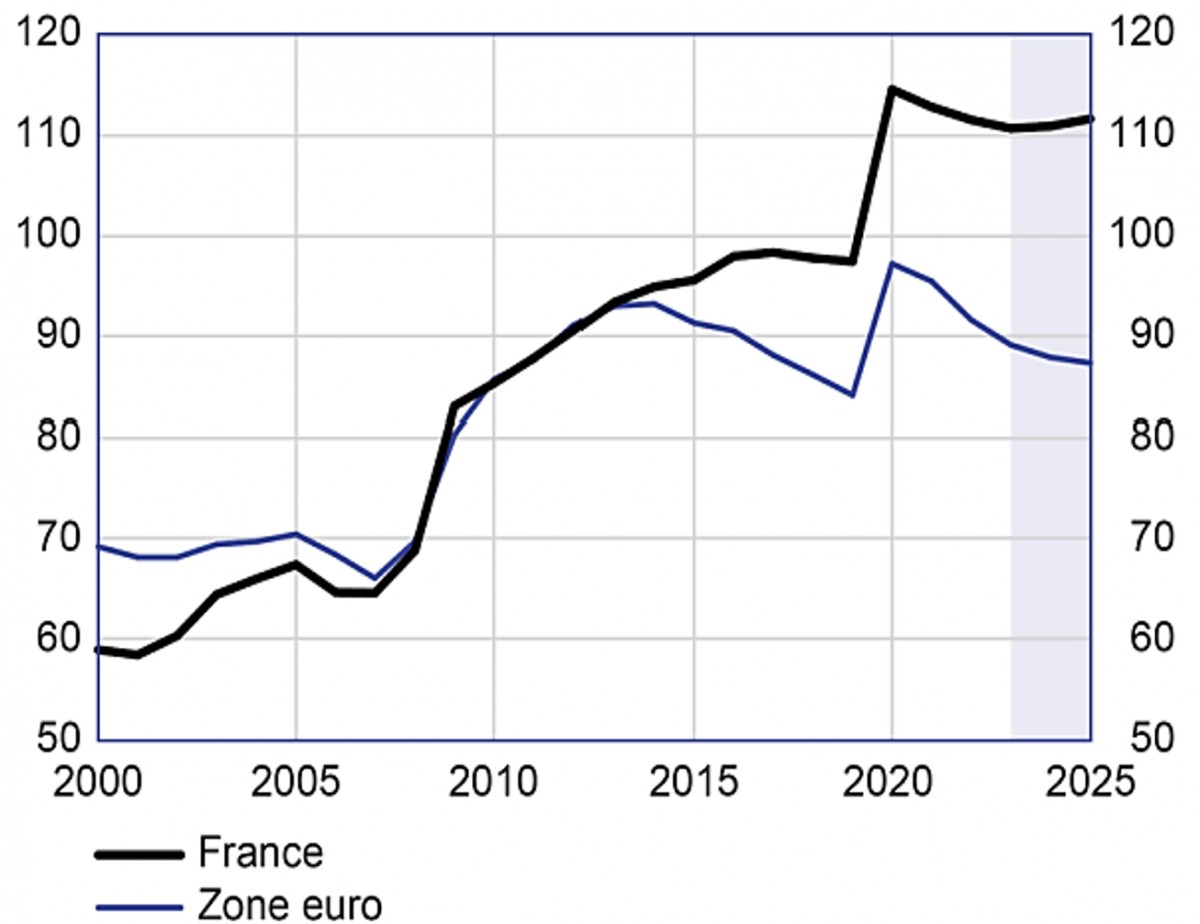

Notwithstanding, the question arises as to whether debt reduction should be such a priority and whether, in the specific case of France, it is feasible to achieve this goal without destabilising the economy. According to the latest projections by the Banque de France, the public deficit is estimated to be around 4.5% by 2025, with Debt/GDP levels similar to current levels, as shown in the graph. This contrasts significantly with data from the rest of the Eurozone, which show a much more optimistic outlook and indicate that other governments have shown a real commitment to this target.

Moreover, all other things being equal, the savings generated by the progressive abandonment of the recovery measures will go to other equally or even more important items of expenditure in the long term, namely the Estrategia Francia 2030 and the so-called Fonds Vert. These projects, which undoubtedly deserve a more in-depth and detailed analysis in the coming weeks, aim to revolutionise both the productive system and the social infrastructure at the national level. On the one hand, the first aims to place France at the forefront of industrial independence within the EU, generating a fully decarbonised industry with a high value added. At the same time, the Fonds Vert focuses on the adaptation of cities and small municipalities to the ecological transition, promoting the self-sufficiency of buildings (refurbishment, energy independence, etc.), habitability, waste management, traffic management, etc.

It is estimated that for the Estrategia 2030 alone around €30 billion will be allocated, half of which must be earmarked to encourage the decarbonisation of industry. One of its fundamental aspects is to establish an efficient small modular reactor (SMR) industry, which would ensure an adequate energy supply for the country by taking advantage of the investments in nuclear research made since the 1960s. It also aims to lead the world in the production of green hydrogen by the 2030s. These achievements, together with the above, would position France as a strong, energy self-sufficient and highly competitive economy.

It is therefore difficult to believe that the modernisation of French industry can be carried out at the same time as an austere and restrictive fiscal policy whose sole objective is to reduce debt, which does not mean that policies linked to growth must necessarily be inefficient in terms of spending and irresponsible in terms of management. The return of industrial policy implies that states must commit themselves and adopt an active role, as Roy Cobby, Clara García, and Rafael Fernández Sánchez have analysed, and this will sooner or later force the Macron administration to get down to work, decide what it wants to do, and explain in detail what exactly the plan is. In short, it will have to decide whether to jump on the bandwagon and lead the European industrial transition in the long term or persist with the idea that the only way to reduce public debt is to reduce spending and not to increase revenue. In the end, 2027 is just another hurdle in this long-distance race, but in order to overcome it, it is necessary to convince and, above all, to empathise with those whom you have disappointed.

Figure 1.- Debt/GDP levels in the Eurozone and sustainability risks in 2021

Source: Banque de France.

Note: The colours correspond with the associated risk of debt sustainability, for which countries with debt levels inferior to 60% are not always classified as "secure". The scale is the following: Orange, elevated risk; Yellow, moderate risk; Green, low risk.

Note: The colours correspond with the associated risk of debt sustainability, for which countries with debt levels inferior to 60% are not always classified as "secure". The scale is the following: Orange, elevated risk; Yellow, moderate risk; Green, low risk.

[Recibe los análisis de más actualidad en tu correo electrónico o en tu teléfono a través de nuestro canal de Telegram]

Debt targets are indeed important for the Macron administration and partly explain its refusal to give ground in the face of the pension reform protests that pushed parliamentary life to the limit and nearly cost the prime minister her job. The Bercy meeting therefore left us with some interesting points, although it gave little room for collective surprise.• Return to the 3% public deficit track.

• Bring the debt down from 111.6% to 108.3% by 2027.

• Phasing out the expansionary packages put in place to alleviate the effects of COVID-19 and the energy market crisis in 2022.

• A reduction in public spending that does not involve raising taxes on households, with the intention of not affecting household purchasing power.

The statements by Le Maire and Borne send a message to Brussels and their European colleagues: the commitment to the new EU fiscal governance rules is clear. Everything indicates, therefore, that the government intends to fly the flag of responsible management in the face of the effervescence of the political left and the aggressiveness of the Rassemblement National, which is the real opposition in parliament and the rival to beat in 2027.

Figure 2.- The evolution of French debt with respect to the average debt in the Eurozone (% of GDP)

Source: Banque de France, Macroeconomic Projections June 2023

Notwithstanding, the question arises as to whether debt reduction should be such a priority and whether, in the specific case of France, it is feasible to achieve this goal without destabilising the economy. According to the latest projections by the Banque de France, the public deficit is estimated to be around 4.5% by 2025, with Debt/GDP levels similar to current levels, as shown in the graph. This contrasts significantly with data from the rest of the Eurozone, which show a much more optimistic outlook and indicate that other governments have shown a real commitment to this target.

Moreover, all other things being equal, the savings generated by the progressive abandonment of the recovery measures will go to other equally or even more important items of expenditure in the long term, namely the Estrategia Francia 2030 and the so-called Fonds Vert. These projects, which undoubtedly deserve a more in-depth and detailed analysis in the coming weeks, aim to revolutionise both the productive system and the social infrastructure at the national level. On the one hand, the first aims to place France at the forefront of industrial independence within the EU, generating a fully decarbonised industry with a high value added. At the same time, the Fonds Vert focuses on the adaptation of cities and small municipalities to the ecological transition, promoting the self-sufficiency of buildings (refurbishment, energy independence, etc.), habitability, waste management, traffic management, etc.

It is estimated that for the Estrategia 2030 alone around €30 billion will be allocated, half of which must be earmarked to encourage the decarbonisation of industry. One of its fundamental aspects is to establish an efficient small modular reactor (SMR) industry, which would ensure an adequate energy supply for the country by taking advantage of the investments in nuclear research made since the 1960s. It also aims to lead the world in the production of green hydrogen by the 2030s. These achievements, together with the above, would position France as a strong, energy self-sufficient and highly competitive economy.

It is therefore difficult to believe that the modernisation of French industry can be carried out at the same time as an austere and restrictive fiscal policy whose sole objective is to reduce debt, which does not mean that policies linked to growth must necessarily be inefficient in terms of spending and irresponsible in terms of management. The return of industrial policy implies that states must commit themselves and adopt an active role, as Roy Cobby, Clara García, and Rafael Fernández Sánchez have analysed, and this will sooner or later force the Macron administration to get down to work, decide what it wants to do, and explain in detail what exactly the plan is. In short, it will have to decide whether to jump on the bandwagon and lead the European industrial transition in the long term or persist with the idea that the only way to reduce public debt is to reduce spending and not to increase revenue. In the end, 2027 is just another hurdle in this long-distance race, but in order to overcome it, it is necessary to convince and, above all, to empathise with those whom you have disappointed.

Se puede leer el artículo original en español en Cinco Días

ARTÍCULOS RELACIONADOS

.jpg)

Miguel Ángel Ortiz-Serrano

Profesor de Historia de la Empresa en CUNEF Universidad.

Es doctor en Historia Económica por la Universidad Carlos III de Madrid y fue profesor de Economía en la Universidad de Sussex (Reino Unido). Ha desarrollado el grueso de su actividad investigadora en Sciences Po Paris, donde se ha especializado en el estudio de los mercados financieros en Francia y Europa a finales del siglo XIX.

Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 171 semanas

Macron Seems To Have Lost His Mind!

Hace 173 semanas

Why Emmanuel Macron Should Withdraw His Pension Reform Bill

Lo más leído