Germany in Recession: What are the causes, and what does it mean for the European Union?

1- The development of the German economy has been very positive in recent decadesGermany is the fourth largest economy in the world in terms of GDP, after the USA, China, and Japan, and far ahead of other Eurozone economies such as France, Italy, and Spain or even economic giants such as India. It is also the most populous member state of the European Union, with more than 84 million inhabitants. Popularly, Germany is known as the economic locomotive of Europe.

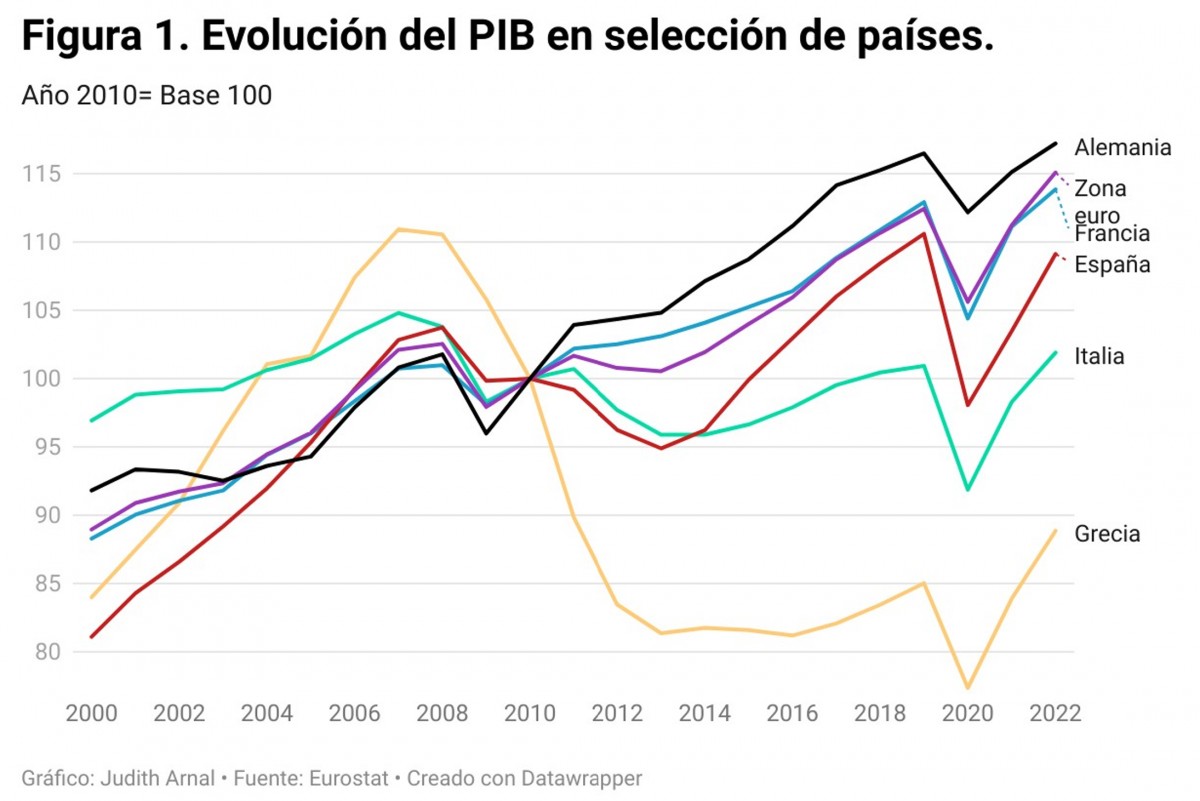

But Germany has not always been in a position of privilege or strength. In the late 1990s and early 2000s, Germany, in the midst of absorbing the consequences of the country’s reunification, was known as the economic sick man of Europe. However, as shown in Figure 1, it re-emerged strongly and significantly changed its geo-economic position, which allowed it to play a decisive role in the eurozone sovereign debt crisis. Thus, when countries such as Greece, Portugal, Ireland, and Cyprus lost access to financial markets, Germany found itself in a strong position to largely dictate the economic conditionality that these Member States had to meet in exchange for receiving the public funds necessary to cover their gross financing needs.

Figure 1.- GDP Growth in a Selection of Countries

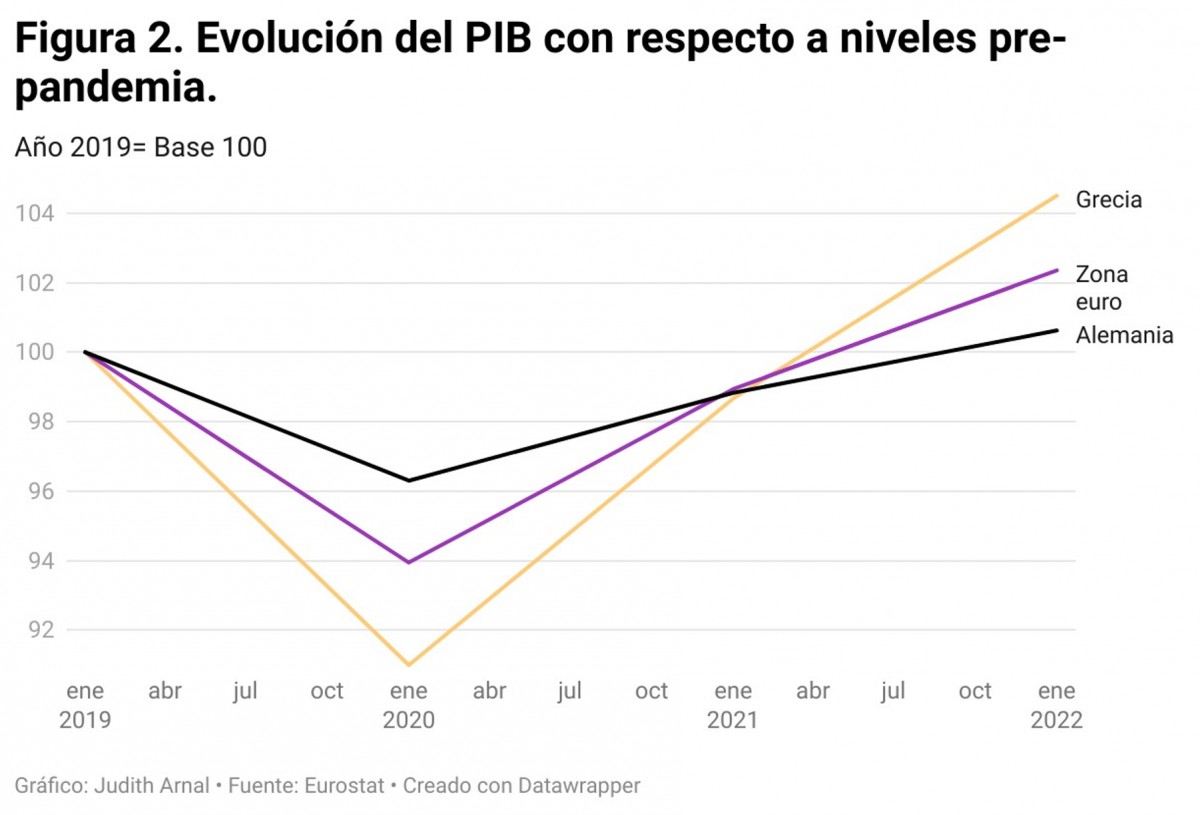

2- The resilience of the German economy has started to break downHowever, this resilience of the German economy seems to be cracking. Germany is probably facing its biggest economic challenge since reunification in the 1990s. As shown in Figure 2, the pace of the return of German GDP to the pre-pandemic level is substantially slower than in the euro area average or even in Greece, traditionally considered the weakest link in the single currency area.

Figure 2.- GDP Growth with Respect to Pre-Pandemic Levels

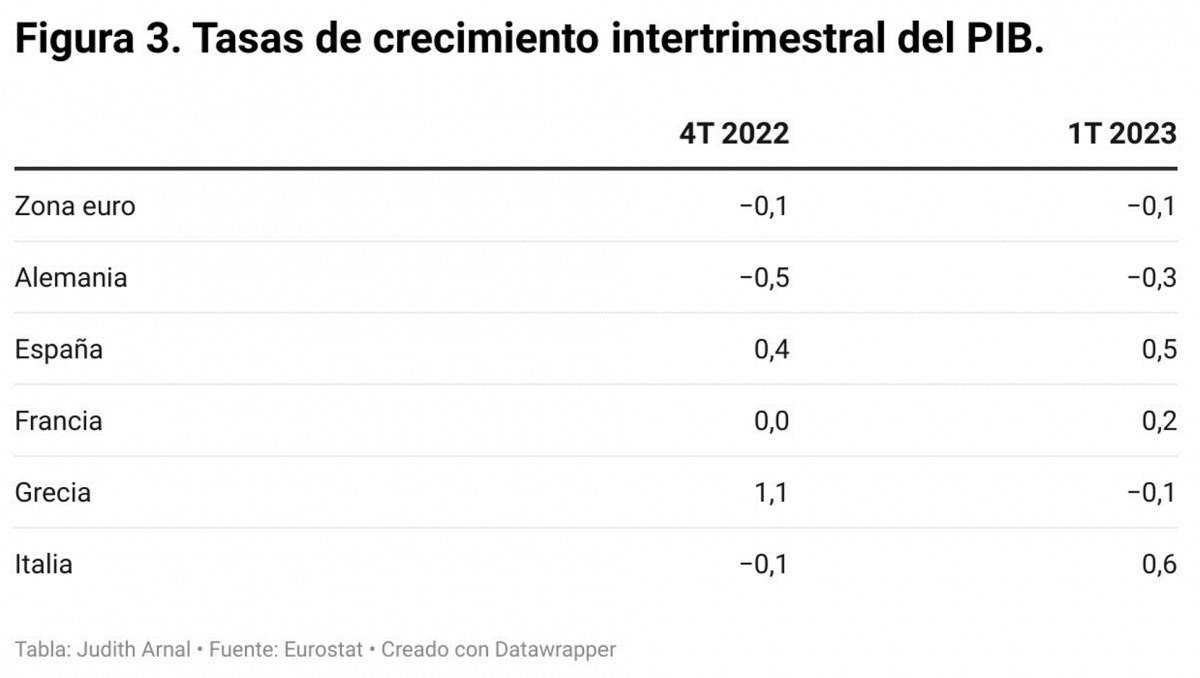

In fact, taking into account GDP growth data for the last quarter of 2022 and the first quarter of 2023, it can be said that Germany has already entered a technical recession (a country enters a technical recession when it accumulates at least two consecutive quarters of negative GDP growth), which contrasts with other large euro area Member States, as can be seen in Figure 3. The strong weight of the German economy on the euro area as a whole also has led to the eurozone itself entering a recession. Moreover, according to the IMF’s Spring World Economic Outlook, Germany will be the only EU economy with a negative GDP growth rate in 2023.

Figure 3.- Quarterly GDP Growth Rates

Analysing the composition of German economic growth in the first quarter of 2023, it can be seen that the factors that weighed negatively are both household consumption and government final consumption. On the other hand, investment and the foreign sector contributed positively. In particular, household consumption fell by 1.2% quarter-on-quarter, especially in food and beverages, clothing and footwear, furniture and automobiles – the latter probably due to the end of subsidies for hybrids and electric cars. Government final consumption also fell sharply, by 4.9%, from the previous quarter. By contrast, investment performance was very positive: construction investment grew by 3.9% and capital and machinery investment by 3.2%.

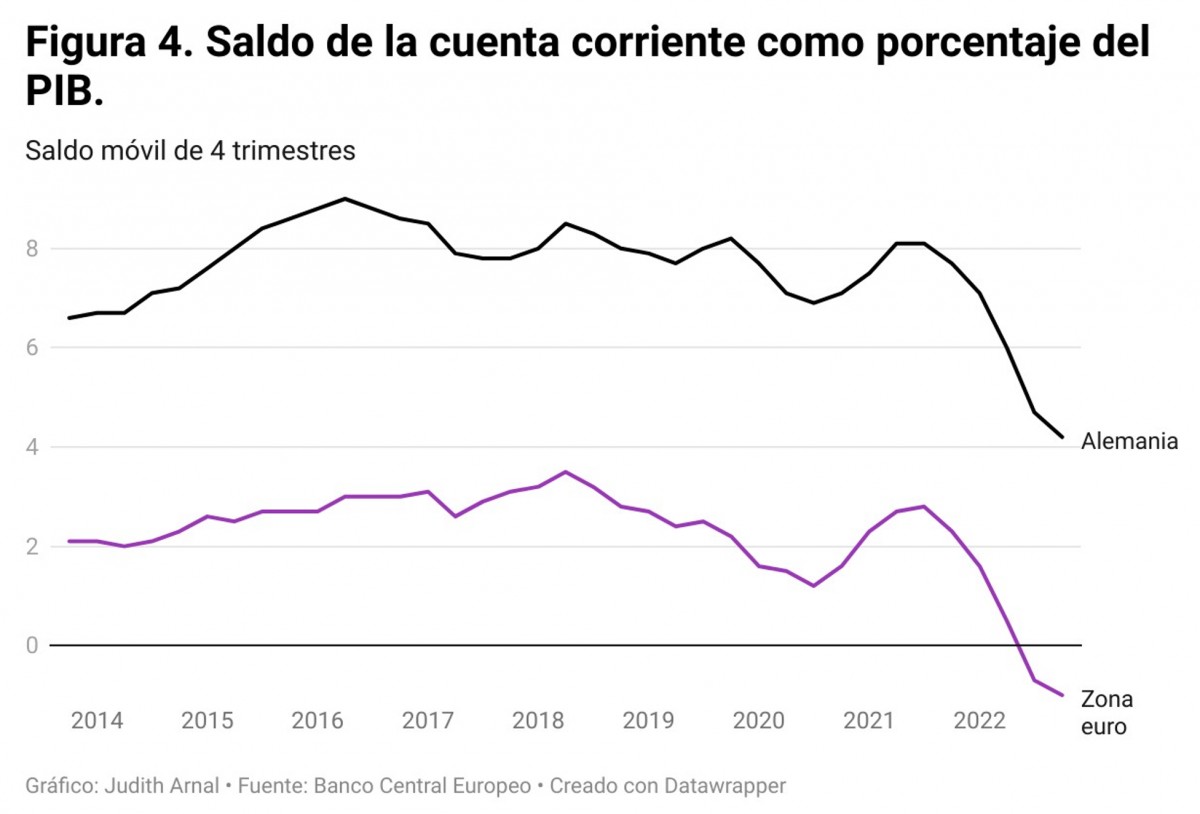

Figure 4.- Current Account Balance (% of GDP)

Business expectations for Germany are not positive. For example, the Ifo Business Climate Index fell in May for the first time in six months to 91.7 points from 93.4 points in April. Expectations about the business climate are particularly negative in the manufacturing sector, irrespective of industry, and in trade, especially wholesale trade.

3- The pillars of the German economyIn order to make a good diagnosis of the reasons that have led the German economy into recession, it is useful to explain first of all what the pillars of the Teutonic economy are. They are essentially four: (1) industry, (2) the foreign sector, (3) the strength of medium-sized companies (the so-called Mittelstand) and (4) the good functioning of logistics and transport operators and a first-rate infrastructure network.

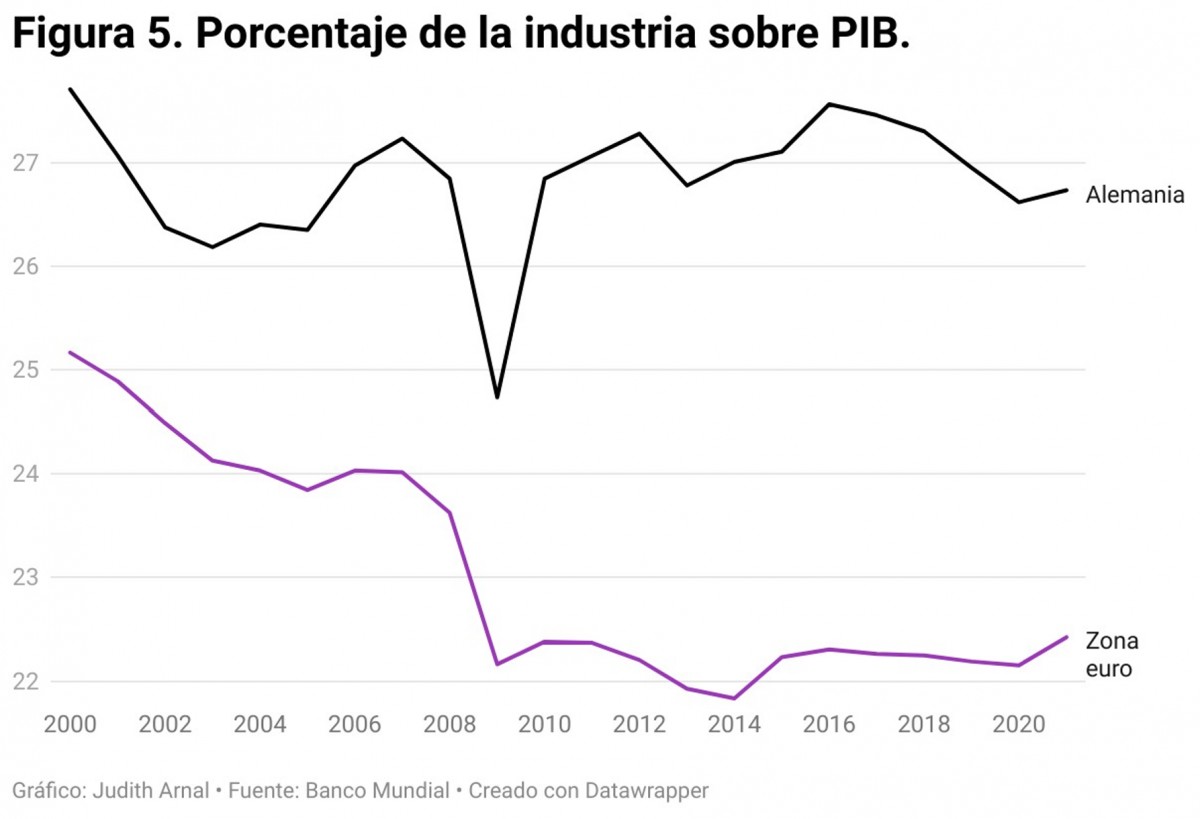

The German economy is characterised by the importance of its industrial sector, which accounted for almost 27% of GDP in 2021, compared to just over 22% in the euro area. This share has been fairly stable over the last 20 years, with the exception of a drop linked to the 2008 crisis, as shown in Figure 5. The strongest industrial sectors in Germany are automotive, mechanical and electrical engineering, chemicals, pharmaceuticals, and agri-food.

Figure 5.- Industry (% of GDP)

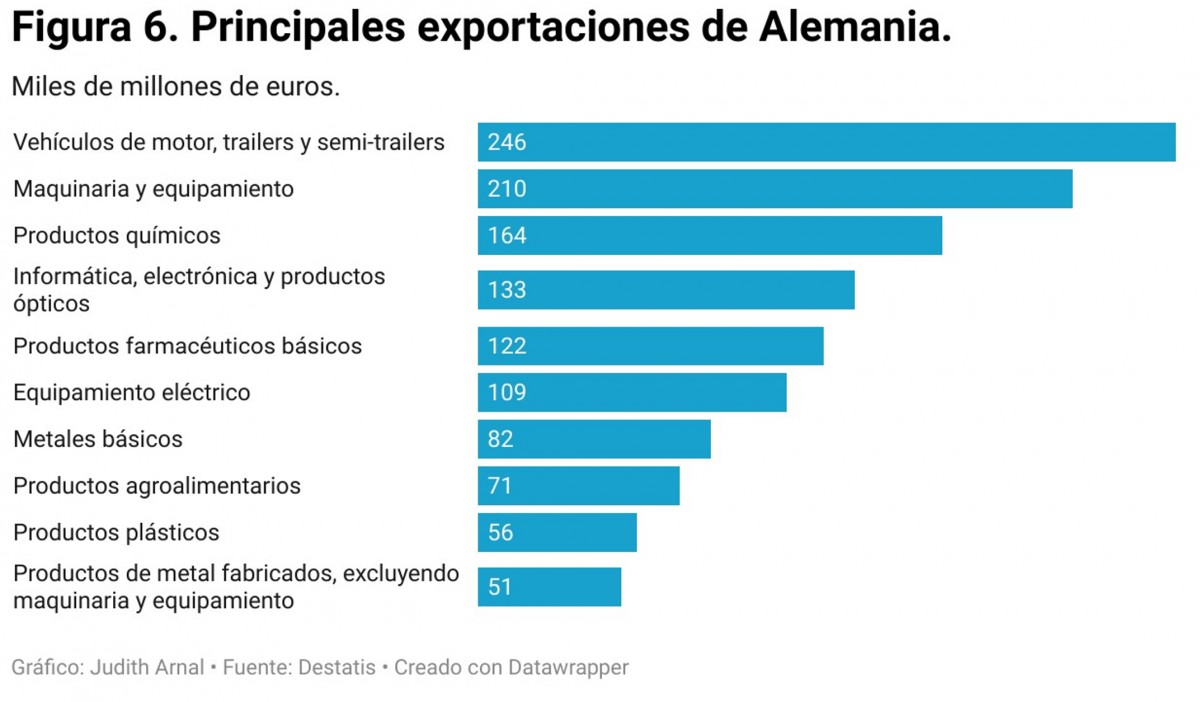

Figure 4, while showing a worsening of Germany’s current account balance, is in turn good evidence of the strength of its external sector. And Germany’s foreign sector is thriving precisely because of its leading-edge industry. As Figure 6 shows, Germany’s main exports are industrial products.

Figure 6.- Top Exports of Germany

German foreign trade is characterised by its strong international dimension. Trade, both in terms of exports and imports, with the other EU countries is below 50%. As shown in Figure 7, Germany’s main trading partners in 2022 were China (with a total trade volume of €299 billion) and the USA (€248 billion). This distribution of trading partners shows how fully integrated Germany is in global value chains. In 2022, China was Germany’s largest trading partner for the seventh year in a row. China is crucial for Germany in terms of imports, being the key supplier of rare earths, which are indispensable for the production of batteries and semiconductors. Proof of China’s importance for Germany is that the chemical giant BASF has invested €10 billion in a new factory in southern China. But China is also important for Germany as a market for its products: for example, Volkswagen, Europe’s largest car manufacturer, places 40% of its production volume in China.

Figure 7.- Top Trade Partners of Germany in 2022

The third pillar of the German economy is the strength of medium-sized enterprises (the so-called Mittelstand). Thanks to the Mittelstand, Germany has a very dense network of medium-sized enterprises, often with a family tradition. The Mittelstand allows economic activity and employment to be spread throughout the country, even in small localities.

Finally, Germany has first-class transport and logistics operators, as well as an excellent infrastructure network. These include DB Schenker and Deutsche Post DHL. Hapag Lloyd in container transport and Lufthansa Cargo and DHL in air transport should not be forgotten. Germany’s transport infrastructure is also first class. The port of Hamburg is the third largest in Europe in terms of container traffic, and the airports of Frankfurt and Leipzig rank first and third in Europe respectively as freight airports. The port of Duisburg is the leading inland waterway port in Europe. Germany also ranks first in road and rail freight transport.

4- The reasons for the negative trendBeyond knowing that the factors that have weighed negatively on the evolution of GDP in the first quarter of 2023 are household consumption and government final consumption, it is worth carrying out a more in-depth analysis to determine what might be behind this trend.

Basically, in recent years, the actions of the Russian, Chinese, and US governments have damaged the pillars of the German economy. The invasion of Ukraine, China’s rigidity, and rising US protectionism are affecting Germany’s economic growth model. In a multilateral world in which the rules of the World Trade Organisation were fully respected, the German economy would have no major problems. But the fact is that the geopolitical situation has changed dramatically in recent times.

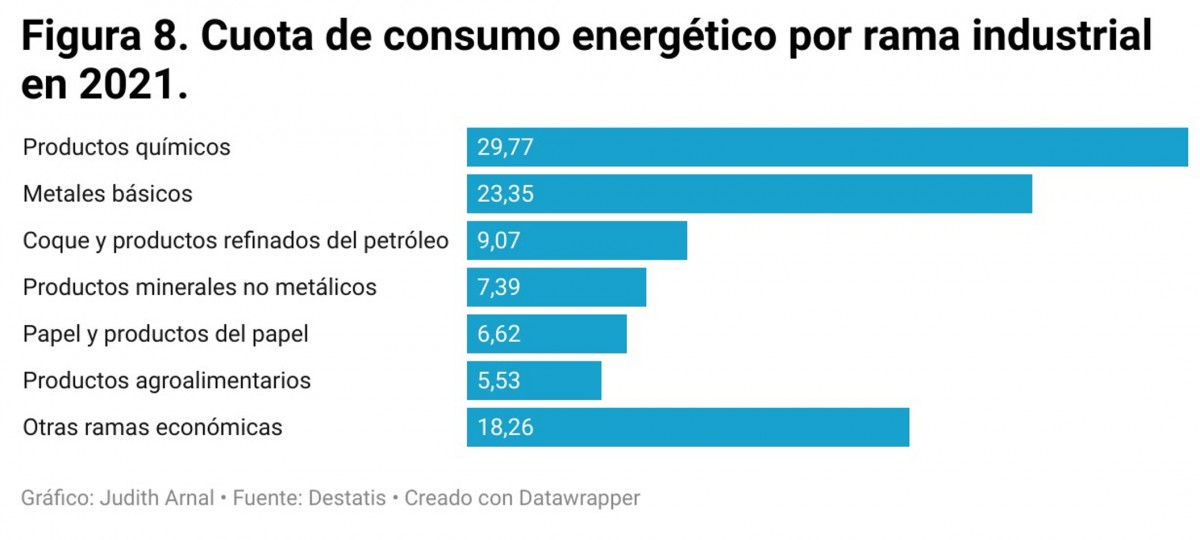

Until Russia’s invasion of Ukraine, Germany had benefited from reasonably priced imported energy. A possible miscalculation on Germany’s part has been to consider energy from a purely commercial perspective, as just another input in its production process, without perceiving its strategic nature and the advantageous use that its supplier (Russia) could make of it. The sharp rise in energy prices is a particular problem for Germany, as much of its industry is highly energy-dependent. Figure 8 gives an idea of the relative importance of energy consumption by industry.

Figure 8.- Share of Energy Consumption by Industrial Sector in 2021

The current easing of energy prices is undoubtedly a relief for the German economy, but the situation is far from ideal. In 2020, Germany’s energy dependency ratio exceeded 63%, compared to the EU average of 57.5%. Moreover, coal remains the main energy source for electricity production in Germany, as shown in Figure 9. The situation of energy dependency has been aggravated, at least temporarily, by the decision to phase out nuclear power for good. This is a striking decision, especially in light of the fact that nuclear energy plays a key role in the energy mix of other large Member States such as France, and that yet another energy source is being dispensed with at a sensitive time.

Figure 9.- Germany's Energy Mix in Terms of Electricity Generation

For several years now, China has been an ally, a competitor and a systemic rival for the West. The elements of competition and rivalry have increased in recent years, but it is undeniable that China remains an ally without which many global challenges could not be met. Germany is well aware of this situation and has in fact reflected this in its National Security Strategy, published on 14 June. As explained above, China is Germany’s main trading partner, and dependence is particularly strong on some critical raw materials. It is a difficult relationship to manage, but the experience with Russia and energy has been a wake-up call that is already leading to action, both at the national level in Germany and at the EU level.

What has perhaps been most surprising about the situation has been the protectionist policy of the US, clearly embodied in the Inflation Reduction Act, passed under a Democratic administration. Although the subsidies contained in the US Inflation Reduction Act are not quantitatively higher than those in the EU, the situation is potentially very pernicious for the EU bloc and for powers such as Germany for three reasons: (1) many of the US subsidies consist of tax credits, which are much easier to implement; (2) access to subsidies is not as bureaucratic as in the EU, making it easier for companies and consumers; (3) the US subsidy package contains a number of protectionist clauses ("Buy American"), whereby only products that have been produced in the US to a very high degree are eligible for subsidies. This is already being felt in individual cases. One example: the electric car manufacturer Tesla announced in February of this year that it was abandoning its plans to build its largest battery factory near Berlin, preferring to focus on the US market. Another example: the German business federation BDI conducted a survey according to which 16% of the Mittelstand companies interviewed had initiated steps to relocate part of their business, while another 30% were considering doing so. Yet another example: Germany has been forced to increase the subsidy to Intel from €6.8 billion to €10 billion in order to retain the project to build a chip factory in Magdeburg.

But the current situation is not only due to geopolitical circumstances, such as those mentioned above, or to a misperception of the strategic nature of energy for an economy that is so dependent on energy-intensive industry. Indeed, the German economy faces more structural challenges, such as in the areas of digitalisation, education, and demographics. In the area of digitalisation, Germany clearly punches below its weight. For example, according to the Digital Economy and Society Index (DESI) for 2022, which summarises indicators on digital development and progress in the EU Member States, Germany ranked a modest thirteenth, behind other large Member States such as Spain and France and only slightly above the EU average. Another example: the percentage of households covered by ultrafast broadband above 1 Gigabyte in 2021 was 62.1% in Germany, compared to 92.5% in Spain. In terms of training, Mittelstand companies are facing a serious shortage of access to skilled personnel, so necessary to continue innovating. And what about the impact of the progressive ageing of the population, a problem endemic to European society in general.

5- Implications for the European Union and next stepsGermany’s importance for the economic development of the rest of the EU and the eurozone is beyond doubt. Some see with joy that Germany has entered recession and that the EU’s growth engine now seems to reside in the so-called peripheral countries. However, this cannot be a cause for celebration at all.

In 2021, Germany was the largest trading partner for exports of goods for 16 EU Member States. Even for Member States that were not among those 16, the links with Germany are undeniable. By way of example, Spain’s main trading partner in terms of exports of goods is France, but in turn, France’s main trading partner is Germany. From the perspective of imports of goods, Germany was also the main trading partner for 16 Member States. And again, for those Member States that were not among these 16, the main trading partner in imports of goods was a neighbouring state of Germany. For example, for Spain, the main trading partner in terms of imports of goods is the Netherlands. This being the case, if Germany’s engine is on the fritz, it is only a matter of time before the rest of the Member States suffer as well.

The fact that Germany’s business cycle is not synchronised with that of the rest of the euro area may also make it difficult for the European Central Bank to set the optimal monetary policy stance.

Therefore, far from rejoicing that Germany’s economic situation is now not the best and thinking that investments that would otherwise have gone to Germany can be attracted, the other EU Member States must try to pull their weight. While it may have seemed to some that the German position was very tough during the eurozone’s sovereign debt crisis, the fact is that very significant progress was made in the Economic and Monetary Union project. This is not to say that the handling of the sovereign debt crisis was without mistakes or room for improvement (the suffering imposed on the Greek people was undoubtedly unnecessary), but Germany made important concessions. The launch of the Next Generation EU in response to the pandemic was also a moment of EU high thinking, which mainly benefited the countries most affected by the pandemic (Italy and Spain), but without Germany’s approval and drive, this initiative would never have gone ahead. Germany is thus a key partner for the EU, in fact, it is its locomotive. Any impulse that can be given to Germany from the EU or the other Member States must be pursued without hesitation.

Although the challenges are significant, there is considerable room for optimism. The weaknesses of the German economy have been identified by its authorities. Diagnosing the disease is a sine qua non for curing it. While it is true that there are three voices in the German coalition government (Social Democrats, Liberals, and Greens) with very different sensitivities and opinions, it is also true that they have already set to work to adopt important reforms to tackle the challenges outlined above. And it should not be forgotten that if there is one EU member state accustomed to rising phoenix-like from traumatic situations, it is Germany.

Se puede leer el artículo original en español