Martes, 28 de julio de 2026

The Recovery Plan, Year Three

EDUARDO PARRA (EUROPA PRESS)

On Tuesday 6 June, the Council of Ministers approved the addendum to the extension of the Recovery, Transformation, and Resilience Plan, which extends the Plan submitted in 2021 and which must also be approved in the next three months by the European Commission, as the managing authority of the Next Generation EU (NGEU) fund created in 2020 in the context of COVID-19. Spain plans to request €84 billion in loans and allocate €7.7 billion in additional subsidies from the NGEU distribution that correspond to Spain. It also plans to allocate 2,586 funds to Spain under the RepowerEU package, created in the wake of the Ukraine crisis.

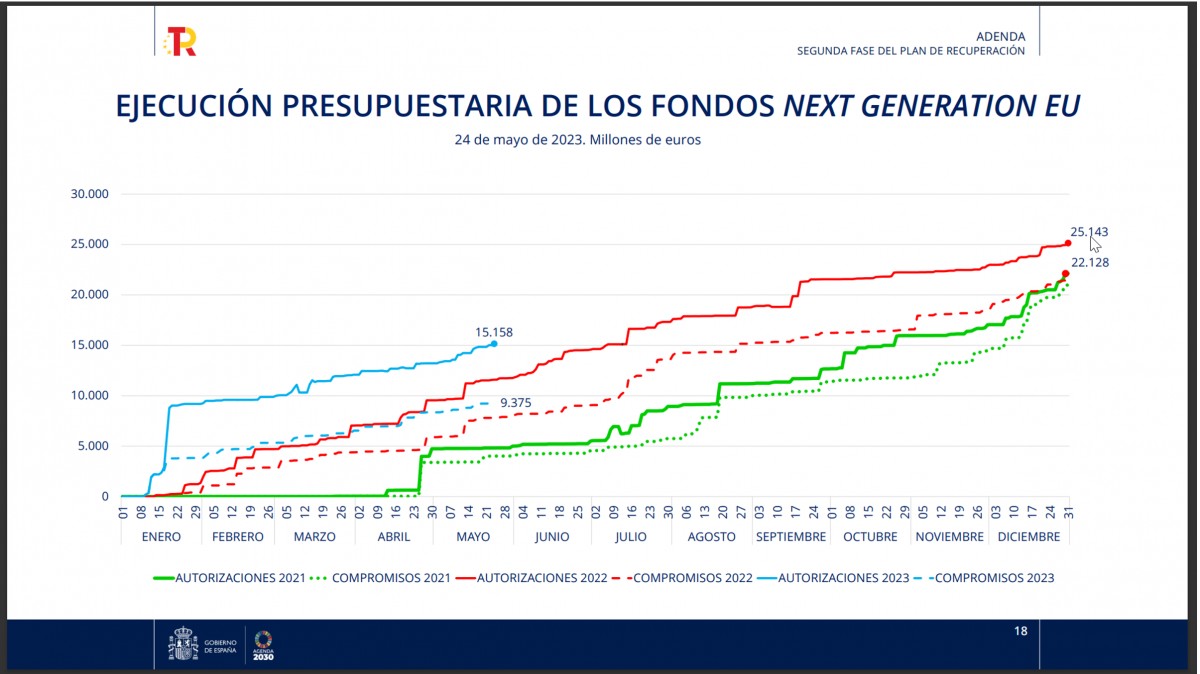

These €10 billion in additional subsidies and, for the first time, €84 billion in Next Generation credits, are in addition to the €69.5 billion in transfers initially allocated to Spain. This would mobilise the total of the €160 billion allocated to Spain for its recovery plan. The Commission has already made three payments totalling €37.036 billion, in exchange for the fulfilment of a series of structural reforms (mainly the approval of new laws, such as the labour reform, the civil servant civil service, and even the first Law for the Evaluation of Public Policies). This accounts for 53% of total planned subsidies. And it contrasts with France, the Netherlands and even Poland whose plans are either not launched or in the initial phase. Most of the others are at 30% of implementation.

Source: Addendum to the Recovery Plan

Source: Addendum to the Recovery Plan

This Next Generation EU funding package (the main element of which is the Recovery and Resilience Mechanism, RRM) is a milestone with its more than €800 billion (just under half in direct grants and the other half in loans): it is twice the size of the traditional Structural Funds. And there is an even more important milestone: it is financed by joint EU borrowing, rather than by transfers from Member States, which for many years has been a taboo for net contributor Member States.

The Recovery Plan is therefore a gamble and a large-scale experiment with enormous consequences for the future. Spain is, after Italy (€191 billion in total, €69 billion in grants), the second largest recipient of funds. The COVID-19 crisis was thus an opportunity, almost an excuse, to try out a new way of making European public policy, as most of the investments in the Recovery Plan have little to do with the pandemic - most of the distribution of funds among member states was made on the basis of 2019 population, GDP and unemployment data. It has much more to do with the pressing need to address and finance major structural reforms, agreed and each year missed by governments during the so-called European Semester, and for which the incentive of the traditional Structural Funds has visibly not been sufficient. The success, or failure, of the Recovery Plan, particularly in Spain and Italy, will have enormous consequences for the future post-2027 budget and European integration itself.

Spain, unlike Italy - more accustomed to high indebtedness - was from the outset reluctant to grant the Recovery Plan in the form of loans. Let us recall that the proportion of these - finally just over half - was the battleground in the exceptional five-day European Council (frugal states versus the rest) in July 2020. Spain and Italy had asked early in the COVID crisis for a direct subsidy to meet the immediate costs of the pandemic and in particular the ERTEs. The SURE (European instrument for temporary Support to mitigate Unemployment Risks in an Emergency) credit line had already been agreed in spring 2020 for precisely this purpose, which was already an important milestone as its almost €100 billion in credits (€21.424 billion for Spain) were also provided on the basis of debt recourse by the European Commission.

In just a few months, therefore, the Next Generation EU represented an enormous qualitative leap in size and shared risks, not only because of the recourse to Community debt but also because of the creation of “European taxes” ('new own resources', in European jargon), initially taxes on emissions, less green imports from outside the EU and on multinationals’ transactions, but which are insufficient to pay off the debt incurred over the last three years until the end of 2058.

Spain, and specifically the government, made the rapid deployment of Next Generation the leitmotiv of its mandate.

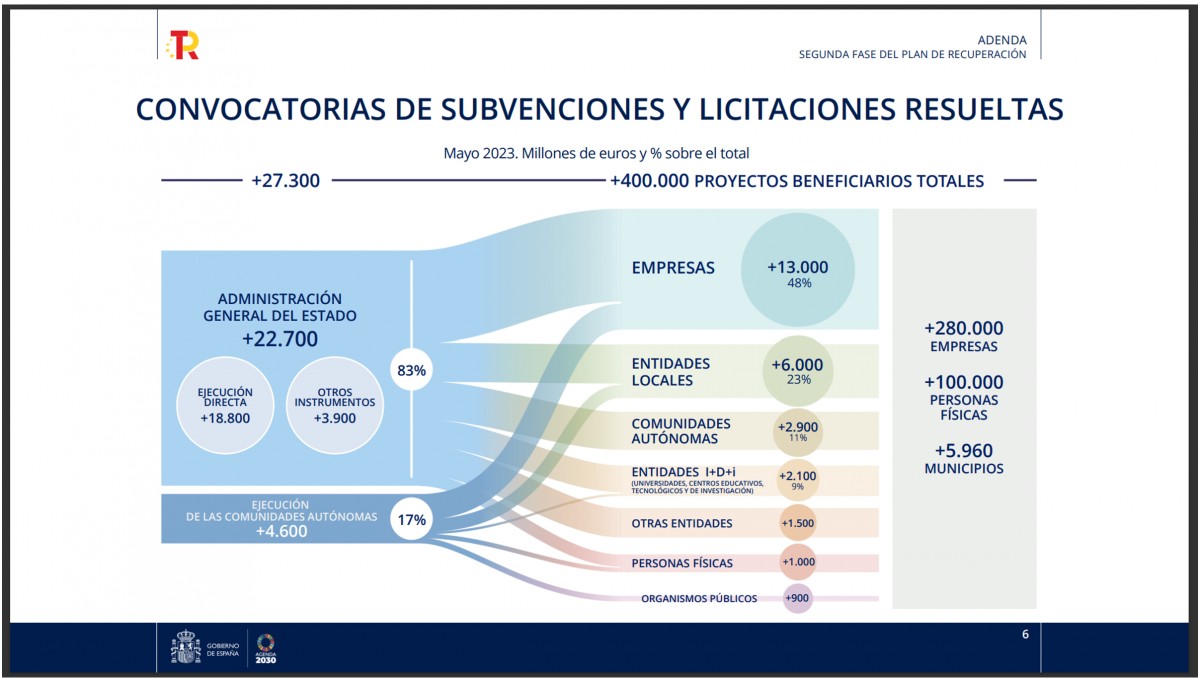

The news and political focus in Spain have been enormous, comparable only to the first arrival of European funds in 1986. The different steps in the drafting and negotiation of the plan dominated the front pages of newspapers and their opinion columns. It has also been revealing of the politicisation of internal intergovernmental relations. Communities such as Euskadi and Galicia each asked for the equivalent of 20% of the total MRR grants. The October 2020 Conference of Presidents with the participation of Commission President Ursula Von der Leyen turned into a sad spectacle of recriminations between territories and towards the government. Co-governance, Iván Redondo’s term for what for decades has been known as multilevel governance, was in principle heavily weighted towards the management of funds by the government, including many ministries with little experience in managing European funds. This is despite the fact that most of the investments are identical to those made for decades by the Autonomous Regions under the EU’s Regional Policy Structural Funds, of which the Communities manage (only) half. In the end, as with the management of the pandemic, there was a certain degree of accommodation, given the limited capacity of the central government to absorb so many funds, and the position of the regions focused on capturing the maximum amount of funds, regardless of their purpose or relevance.

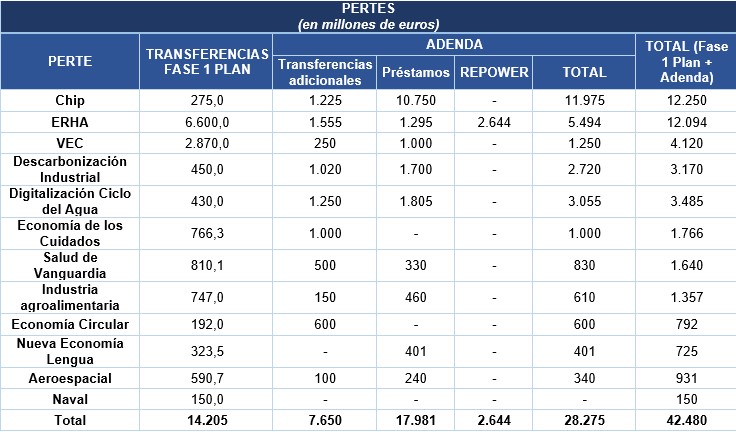

The PERTEs, large public-private partnerships financed in part by the MRR - €14 billion in transfers from the initial Plan - have also been controversial. Their logic of investment in key sectors is framed by the logic of the strategic state, which has also been embraced by the EU. However, the level of executive discretion in the selection, identification and execution of these PERTEs has often been controversial due to the distribution, or not, by regions and the possible capture by economic interests. The addendum foresees an additional €28 billion, of which €10.3 billion from the additional transfers and €18 billion from the new appropriations will be used to reinforce the 12 PERTEs already underway.

Source: Addendum to the Recovery Plan

Source: Addendum to the Recovery Plan

Partisan politicisation has also been very present during the negotiation, approval and start of implementation, including complaints from the opposition regarding the government’s lack of transparency (rejected by the Commission) as well as the partisan instrumentalisation of the highly publicised visit of a delegation of MEPs from the Committee on Budgetary Control. The main confusion is between implementation and transfer. In the case of many initiatives there are data on the transfer to the regions but not, as the MEPs requested, a detailed list of all the beneficiaries. However, the availability of such information is equally difficult for the Structural Funds (less so for the CAP) as evidenced by this study for the European Parliament of the 50 beneficiaries in each country, out of a total of 600,000 beneficiaries across the EU.

The Communities, in addition to the €20 billion in direct subsidies, now benefit from another €20 billion in loans in the so-called Autonomous Resilience Fund for housing, transport or sustainable tourism and the care economy. Predictably, given that not all Autonomous Communities do not have their own Official Credit Institute - not to mention a limited management capacity - the government has decided to entrust the management of the fund to the European Investment Bank, an EU body that has been financing major regional development works for decades, but also since 2007 the so-called financial engineering of cohesion policy, on a much smaller scale (€50 million) for regeneration projects (JESSICA, JASPERS, JEREMIE). The remaining €45 billion will be articulated in 12 credit lines, to reinforce the subsidies granted by the ministries.

Source: Addendum to the Recovery Plan, 2023

Source: Addendum to the Recovery Plan, 2023

In short, despite the doomsayers, the Recovery Plan is going reasonably well.

In any case, Spain’s responsibility is great as the Next Generation EU is a full-scale experiment. It is possible that the implementation of projects will be delayed until 2026 and voices are already beginning to call for an amendment of the MRR Regulation to provide it with the N+3 rule as in the Cohesion Policy. Just in case, the Partnership Agreement and the Regional Structural Fund Programmes (approved in December 2022) are excessively brief, in anticipation of having to take on unfinished NGEU projects by 2026.

Nor is the use by the ‘frugal’ of any problems of irregular execution of funds that may arise in a context in which European fiscal rules (and the political climate) may tighten again.

Moreover, passing a law is not the same as reforming a public policy as a whole, so it will not necessarily result in structural changes that can be evaluated in practice, as external evaluation bodies already fear.

In this respect, more field research on the management of funds is needed. The evidence that occasionally emerges is worrying. Despite the simplification brought about by Royal Decree 36/2020, managers complain about the many changes in the implementation process, the use of cascade subcontracting due to the limited institutional capacity of the administrations, the excessive distribution of small amounts of money through competitive tendering (as in the case of the €10 billion for depopulation).

The Commission itself notes, as in its recent report on territorial convergence and as Bernardo de Miguel points out in Agenda Pública, that the future of Europe once again passes through Spain.

This is something to think ahead of the foreseeably eventful Spanish presidency that begins in July.

These €10 billion in additional subsidies and, for the first time, €84 billion in Next Generation credits, are in addition to the €69.5 billion in transfers initially allocated to Spain. This would mobilise the total of the €160 billion allocated to Spain for its recovery plan. The Commission has already made three payments totalling €37.036 billion, in exchange for the fulfilment of a series of structural reforms (mainly the approval of new laws, such as the labour reform, the civil servant civil service, and even the first Law for the Evaluation of Public Policies). This accounts for 53% of total planned subsidies. And it contrasts with France, the Netherlands and even Poland whose plans are either not launched or in the initial phase. Most of the others are at 30% of implementation.

This Next Generation EU funding package (the main element of which is the Recovery and Resilience Mechanism, RRM) is a milestone with its more than €800 billion (just under half in direct grants and the other half in loans): it is twice the size of the traditional Structural Funds. And there is an even more important milestone: it is financed by joint EU borrowing, rather than by transfers from Member States, which for many years has been a taboo for net contributor Member States.

[Recibe los análisis de más actualidad en tu correo electrónico o en tu teléfono a través de nuestro canal de Telegram]

Moreover, unlike the so-called Territorial Cohesion funds, of which Spain will again receive €36.7 billion until 2027 (and as much for the Common Agricultural Policy and rural development), the MRR grants do not require co-financing (part of the cost of the projects does not have to be financed with own funds). An even more crucial factor: the payment of funds by the Commission is not done through reimbursements once the work or project has been carried out (as with the Structural Funds), but funds are released by the Commission (direct management, and not shared with the states/territories, as in Cohesion policy) depending on the prior fulfilment of a series of milestones. In other words, we are talking about Finance not Linked to Costs (FLNTC), which is also almost unprecedented at EU level. All this makes the Recovery Plan tremendously attractive compared to the 2021-2027 Structural Funds, which have just been launched two years late and whose main comparative advantage is that they can be implemented up to three years later than planned (N+3 rule) while the Recovery Plan funds will have to be implemented by the end of 2026 (with most of the transfers already received by the end of 2023).The Recovery Plan is therefore a gamble and a large-scale experiment with enormous consequences for the future. Spain is, after Italy (€191 billion in total, €69 billion in grants), the second largest recipient of funds. The COVID-19 crisis was thus an opportunity, almost an excuse, to try out a new way of making European public policy, as most of the investments in the Recovery Plan have little to do with the pandemic - most of the distribution of funds among member states was made on the basis of 2019 population, GDP and unemployment data. It has much more to do with the pressing need to address and finance major structural reforms, agreed and each year missed by governments during the so-called European Semester, and for which the incentive of the traditional Structural Funds has visibly not been sufficient. The success, or failure, of the Recovery Plan, particularly in Spain and Italy, will have enormous consequences for the future post-2027 budget and European integration itself.

Spain, unlike Italy - more accustomed to high indebtedness - was from the outset reluctant to grant the Recovery Plan in the form of loans. Let us recall that the proportion of these - finally just over half - was the battleground in the exceptional five-day European Council (frugal states versus the rest) in July 2020. Spain and Italy had asked early in the COVID crisis for a direct subsidy to meet the immediate costs of the pandemic and in particular the ERTEs. The SURE (European instrument for temporary Support to mitigate Unemployment Risks in an Emergency) credit line had already been agreed in spring 2020 for precisely this purpose, which was already an important milestone as its almost €100 billion in credits (€21.424 billion for Spain) were also provided on the basis of debt recourse by the European Commission.

In just a few months, therefore, the Next Generation EU represented an enormous qualitative leap in size and shared risks, not only because of the recourse to Community debt but also because of the creation of “European taxes” ('new own resources', in European jargon), initially taxes on emissions, less green imports from outside the EU and on multinationals’ transactions, but which are insufficient to pay off the debt incurred over the last three years until the end of 2058.

Spain, and specifically the government, made the rapid deployment of Next Generation the leitmotiv of its mandate.

The news and political focus in Spain have been enormous, comparable only to the first arrival of European funds in 1986. The different steps in the drafting and negotiation of the plan dominated the front pages of newspapers and their opinion columns. It has also been revealing of the politicisation of internal intergovernmental relations. Communities such as Euskadi and Galicia each asked for the equivalent of 20% of the total MRR grants. The October 2020 Conference of Presidents with the participation of Commission President Ursula Von der Leyen turned into a sad spectacle of recriminations between territories and towards the government. Co-governance, Iván Redondo’s term for what for decades has been known as multilevel governance, was in principle heavily weighted towards the management of funds by the government, including many ministries with little experience in managing European funds. This is despite the fact that most of the investments are identical to those made for decades by the Autonomous Regions under the EU’s Regional Policy Structural Funds, of which the Communities manage (only) half. In the end, as with the management of the pandemic, there was a certain degree of accommodation, given the limited capacity of the central government to absorb so many funds, and the position of the regions focused on capturing the maximum amount of funds, regardless of their purpose or relevance.

The PERTEs, large public-private partnerships financed in part by the MRR - €14 billion in transfers from the initial Plan - have also been controversial. Their logic of investment in key sectors is framed by the logic of the strategic state, which has also been embraced by the EU. However, the level of executive discretion in the selection, identification and execution of these PERTEs has often been controversial due to the distribution, or not, by regions and the possible capture by economic interests. The addendum foresees an additional €28 billion, of which €10.3 billion from the additional transfers and €18 billion from the new appropriations will be used to reinforce the 12 PERTEs already underway.

Partisan politicisation has also been very present during the negotiation, approval and start of implementation, including complaints from the opposition regarding the government’s lack of transparency (rejected by the Commission) as well as the partisan instrumentalisation of the highly publicised visit of a delegation of MEPs from the Committee on Budgetary Control. The main confusion is between implementation and transfer. In the case of many initiatives there are data on the transfer to the regions but not, as the MEPs requested, a detailed list of all the beneficiaries. However, the availability of such information is equally difficult for the Structural Funds (less so for the CAP) as evidenced by this study for the European Parliament of the 50 beneficiaries in each country, out of a total of 600,000 beneficiaries across the EU.

The Communities, in addition to the €20 billion in direct subsidies, now benefit from another €20 billion in loans in the so-called Autonomous Resilience Fund for housing, transport or sustainable tourism and the care economy. Predictably, given that not all Autonomous Communities do not have their own Official Credit Institute - not to mention a limited management capacity - the government has decided to entrust the management of the fund to the European Investment Bank, an EU body that has been financing major regional development works for decades, but also since 2007 the so-called financial engineering of cohesion policy, on a much smaller scale (€50 million) for regeneration projects (JESSICA, JASPERS, JEREMIE). The remaining €45 billion will be articulated in 12 credit lines, to reinforce the subsidies granted by the ministries.

In short, despite the doomsayers, the Recovery Plan is going reasonably well.

In any case, Spain’s responsibility is great as the Next Generation EU is a full-scale experiment. It is possible that the implementation of projects will be delayed until 2026 and voices are already beginning to call for an amendment of the MRR Regulation to provide it with the N+3 rule as in the Cohesion Policy. Just in case, the Partnership Agreement and the Regional Structural Fund Programmes (approved in December 2022) are excessively brief, in anticipation of having to take on unfinished NGEU projects by 2026.

Nor is the use by the ‘frugal’ of any problems of irregular execution of funds that may arise in a context in which European fiscal rules (and the political climate) may tighten again.

Moreover, passing a law is not the same as reforming a public policy as a whole, so it will not necessarily result in structural changes that can be evaluated in practice, as external evaluation bodies already fear.

In this respect, more field research on the management of funds is needed. The evidence that occasionally emerges is worrying. Despite the simplification brought about by Royal Decree 36/2020, managers complain about the many changes in the implementation process, the use of cascade subcontracting due to the limited institutional capacity of the administrations, the excessive distribution of small amounts of money through competitive tendering (as in the case of the €10 billion for depopulation).

The Commission itself notes, as in its recent report on territorial convergence and as Bernardo de Miguel points out in Agenda Pública, that the future of Europe once again passes through Spain.

This is something to think ahead of the foreseeably eventful Spanish presidency that begins in July.

ARTÍCULOS RELACIONADOS

{kind=link}

Serafín Pazos-Vidal

Senior Expert, Rural and Territorial Development, European Association for Innovation in Local Development (AEIDL) e investigador

Analista de política europea con 20 años de experiencia en Bruselas, incluidos 15 como responsable de política europea de COSLA. Coordinador del Grupo de Expertos en Cohesión Territorial del CMRE (2008-2018) y miembro del Grupo de Expertos en Subsidiariedad del CdR. Autor de 'Subsidiarity and EU Multilevel Governance' (Routledge, 2019).

Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 179 semanas

Towards a Spanish Sovereign Wealth Fund

Hace 166 semanas

The Great Return of Vertical Industrial Policy

Lo más leído