Martes, 28 de julio de 2026

Cohesion and Recovery: The battle of 2027

OLIVIER HOSLET (EFE)

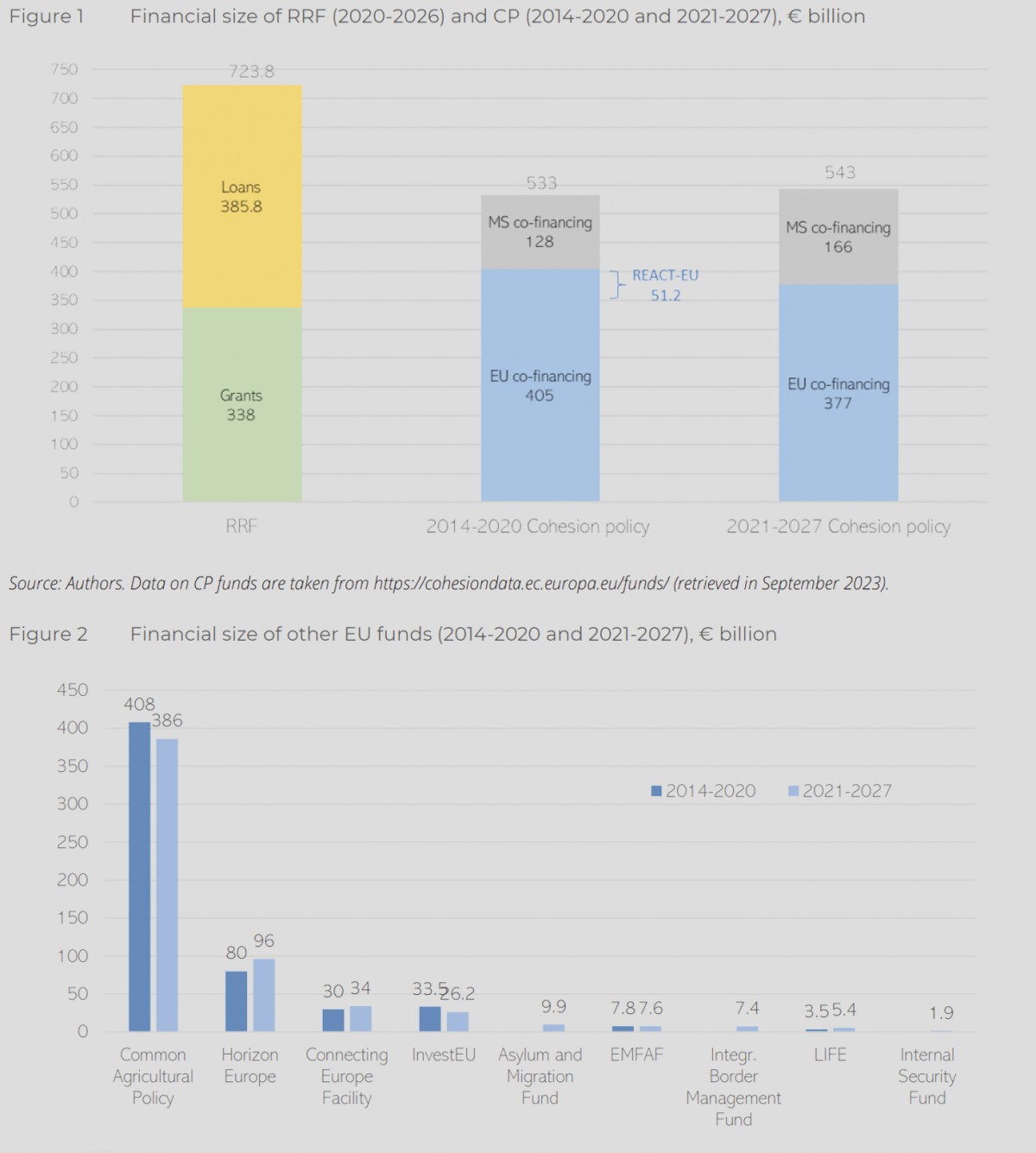

On 21 February, the European Commission presented the results of the mid-term review of the so-called Recovery Plan, formally the Next Generation EU (NGEU) package, and more specifically the Recovery and Resilience Mechanism (RRM). The NGEU, urgently established in July 2020 in the wake of the COVID-19 crisis – and in the genesis of which Spain played a very prominent role –, with €800 billion, almost doubles the EU’s regular multiannual budget for 2021-2027. Of this total, the €650 billion of the RRM makes it the largest fund ever created by the EU - twice as much as the main items in the EU budget, the EU’s Cohesion or Regional Policy and the Common Agricultural Policy. Until the advent of the RRM, the Cohesion Policy – through its Structural Funds – was the largest economic development policy in the world.

To give an idea of the dizzying figures, in Spain the combination of MRRF, regional, rural development, and just transition funds add up to more than €220 billion to be spent between 2021 and 2027, which is in addition to the €15 billion (out of a total of €75 billion) of the 2014-2020 Structural Funds still to be paid.

The Addendum to the Recovery Plan was approved by the Council of Ministers last June and received the go-ahead from the European Commission in October. This means that after the initial reluctance to use only the half of the RRM grants allocated to Spain, the government decided to apply for the €83 billion in loans from the Next Generation EU and RepowerEU funds (an additional package due to the crisis generated by the war in Ukraine), plus €10 billion in additional transfers so that the Recovery Plan alone amounts to €163 billion to be spent in Spain in 2021-2026, more than 12% of Spain’s GDP, in addition to the €36.5 billion from the Structural Funds 2021-2027. Unlike these traditional funds, the MRRF has to be spent one year in advance and does not have the possibility of a 3-year spending extension (N+3), which has foreseeably led to concerns about not being able to spend all the funds allocated, and some timid moves to change the Regulation governing the MRRF.

The European Commission’s Communication on the mid-term review, accompanied by an extensive range of documentation, states that at EU level just under half (€225 billion) of the RRF has already been spent – weighed down by the slow approval of many National Recovery and Resilience Plans, as unlike in Spain – the first and negotiated with enormous public interest and not a little political wrangling – some were only approved in 2023 – in some cases, as in the countries with the best economic data, effectively renouncing the appropriations (€75 billion).

In particular, the external evaluation commissioned by the Commission highlights that EU-wide GDP has been 0.4% higher than it would have been without the RRM spending. It also highlights that, according to the administrations interviewed, many pending structural reforms have been made possible with the impetus of the Recovery Plan.

Source: Corti et al, 2024

Source: Corti et al, 2024

Beyond the numbers, or whether in a context of successive crises the MRR will add almost 1.4% to EU GDP by 2026 (it has certainly been instrumental in bringing public investment across the EU to 3.4% of GDP by 2024), it is necessary to consider that rather than a response to COVID-19, the NGEU has been the long-awaited opportunity to try to overcome three dilemmas.

First and foremost, that the EU budget could be financed not only by transfers from member states (which generates the whole unhealthy dynamic between “frugal” net contributors and beneficiaries) but also by own funds, and through joint borrowing, long a Rubicon that the most prosperous countries refused to cross: NGEU is financed entirely by borrowing, to be paid for by a panoply of new own resources or “European taxes” (emissions taxes, multinational profits, but potentially new taxes on cryptocurrencies or on waste) from 2026; the NGEU is to be paid for until 2058.

Second and no less fundamental is the need for Member States to tackle so-called structural reforms - often internal reforms where EU jurisdiction does not reach, such as pensions or labour market reforms - which they have been promising for two decades in annual National Reform Plans, in the multi-level negotiating process called the European Semester. The problem is that, although the Structural Funds required the fulfilment of certain conditionalities linked to the Semester, in the best of cases these funds would only be a useful lever to carry out these reforms in the most benefited countries.

This connects to the third dilemma: how to make the spending of European funds faster, more efficient and invested in agreed priorities at EU level. The EU’s main investment programme, the Structural Funds, used to be characterised by a very rigid – and multi-level, as much of the spending is managed by territorial administrations – system of multi-annual planning. Expenditure is only reimbursable to the Member State several years after implementation after a very rigorous evaluation of all documentation, and most expenditure must be co-financed by the Member State. Moreover, although evaluation has started to be done not only on the basis of the expenditure incurred but also on the basis of the results achieved, it is still under development. Therefore, the advent of the RRM meant trying something radically new, certainly on this gigantic scale, payment by results, but not linked to costs (Finance Not Linked to Costs) but to the achievement of targets linked to the structural reforms of the Semester committed to in each Recovery Plan. For example, at the end of 2022 an agreement was reached in extremis for labour reform, the urgency of which came about because it was a sine qua non condition for the disbursement of €12 billion of the MRR – and which were spent on projects that mostly have nothing to do with employment policies, something unthinkable in the traditional system.

The Commission’s communication thus states that by the end of 2023 no less than 1,150 milestones have been met by all member states. Certainly, delivering reforms in exchange for money has worked. However, if you look at the Operational Provisions of the Recovery Plan containing the milestones agreed with the Commission by Spain, you will see that they are very general: a milestone can be a result, a result can simply be that a law is passed and implemented. For example, the first Public Policy Evaluation Law was agreed in 2022 with no little haste as it was linked to the payment of one of the tranches of the MRR, and not to the creation – still pending and much needed – of a policy evaluation system in Spain, including that of European funds. The European Court of Auditors has repeatedly sounded the alarm on the major EU-wide weaknesses of such an incipient system, but one to which unprecedented amounts of funds have been allocated. Measuring results at the social level and linking them to concrete expenditure is not easy, especially at this scale.

However, the advantage for the long-suffering administrations is obvious, as management is simpler and the state receives the money in advance, unlike with the Structural Funds. The aforementioned mid-term evaluation of the RRF indicates that, although no evidence has been found of substitution of traditional 2014-2020 funds by the RRF, since it is already underway – and Spain is the furthest behind – it can already be seen that the 2021-2027 Structural Funds will only begin to be spent once it is no longer possible to do so through the Recovery Plan, which could mean that by 2026 – the last year of the RRF – there will be a huge bag of traditional funds to be spent, under the aforementioned N+3, until 2030.

And this, finally, is the ultimate dilemma of the Recovery Plan, being in fact a critique of the Structural Funds. Faster, easier to spend, more result-linked, but much more centralised, even in federal states like Germany, which is unprecedented. In principle the Recovery Plan runs out in 2026, as it was an extraordinary instrument outside the EU budget and financed by debt, although Commission President Von der Leyen – who will probably succeed herself this July – has already threatened to repeat the feat of agreeing the MRR with the Social Climate Fund – presented only two months after the historic NGEU agreement at the four-day summit in July 2020 – and which, after great resistance, will mean that the EU will have to pay the EU budget for the Recovery Plan in 2026, after great resistance, will mean that in 2026-2024 there will be a new €65 million fund (financed by revenues from emissions trading) to finance vulnerable households and the decarbonisation of transport.

Time in Brussels is relative, and while the focus is shifting to the June 2024 elections, in reality the post-2027 is already being thought about, as the Commission’s proposals for the new 2028-2034 budget will be made in May 2025, and will focus much of the political capital of the legislature. In all of this, how much of the MRR will remain after 2026 will be no minor issue, especially with regard to the future post-2027 Cohesion Policy, the first announcements of which have just been made by the High-Level Group led by Rodríguez-Pose. In this group, great emphasis is placed on the persistence of great territorial inequalities and the so-called “development traps” whereby many territories – in Spain there are many – are able to emerge from the lowest part of the GDP per capita table, but are then unable to become competitive territories at the European level, no matter how much EU money is transferred to them.

One of the questions is to what extent Cohesion Policy can be equipped with the new clothes of the RRM without distorting its territorial and multi-level essence – something in which the Recovery Plan suffers, as the Commission’s own Communication admits. As its accompanying study on the relationship between the RRM and the Structural Funds states, both funds finance the same things – and are managed by the same teams – but their intervention logic is different, and their management is highly centralised, as regional authorities have complained.

While it may still be premature to say that Cohesion policy simply needs to be transformed into a new Next Generation post-2027, the coming months will see a battle over what should be the dominant paradigm of the European budget in the coming decades: improvements to traditional funding or significant change, long-term investments versus responses to successive poly-crises, own-fund financing or pooled debt. The recent revision of the traditional budget with cuts to traditional policies to finance spending related to the new war climate, more borrowing, and funds for European technological sovereignty, suggests that while 2020 was a revolutionary year for EU finances, the COVID crisis was only the trigger for more radical changes for the Union of tomorrow.

To give an idea of the dizzying figures, in Spain the combination of MRRF, regional, rural development, and just transition funds add up to more than €220 billion to be spent between 2021 and 2027, which is in addition to the €15 billion (out of a total of €75 billion) of the 2014-2020 Structural Funds still to be paid.

The Addendum to the Recovery Plan was approved by the Council of Ministers last June and received the go-ahead from the European Commission in October. This means that after the initial reluctance to use only the half of the RRM grants allocated to Spain, the government decided to apply for the €83 billion in loans from the Next Generation EU and RepowerEU funds (an additional package due to the crisis generated by the war in Ukraine), plus €10 billion in additional transfers so that the Recovery Plan alone amounts to €163 billion to be spent in Spain in 2021-2026, more than 12% of Spain’s GDP, in addition to the €36.5 billion from the Structural Funds 2021-2027. Unlike these traditional funds, the MRRF has to be spent one year in advance and does not have the possibility of a 3-year spending extension (N+3), which has foreseeably led to concerns about not being able to spend all the funds allocated, and some timid moves to change the Regulation governing the MRRF.

The European Commission’s Communication on the mid-term review, accompanied by an extensive range of documentation, states that at EU level just under half (€225 billion) of the RRF has already been spent – weighed down by the slow approval of many National Recovery and Resilience Plans, as unlike in Spain – the first and negotiated with enormous public interest and not a little political wrangling – some were only approved in 2023 – in some cases, as in the countries with the best economic data, effectively renouncing the appropriations (€75 billion).

In particular, the external evaluation commissioned by the Commission highlights that EU-wide GDP has been 0.4% higher than it would have been without the RRM spending. It also highlights that, according to the administrations interviewed, many pending structural reforms have been made possible with the impetus of the Recovery Plan.

Tables: How the Recovery Plan compares to traditional EU funds

Beyond the numbers, or whether in a context of successive crises the MRR will add almost 1.4% to EU GDP by 2026 (it has certainly been instrumental in bringing public investment across the EU to 3.4% of GDP by 2024), it is necessary to consider that rather than a response to COVID-19, the NGEU has been the long-awaited opportunity to try to overcome three dilemmas.

First and foremost, that the EU budget could be financed not only by transfers from member states (which generates the whole unhealthy dynamic between “frugal” net contributors and beneficiaries) but also by own funds, and through joint borrowing, long a Rubicon that the most prosperous countries refused to cross: NGEU is financed entirely by borrowing, to be paid for by a panoply of new own resources or “European taxes” (emissions taxes, multinational profits, but potentially new taxes on cryptocurrencies or on waste) from 2026; the NGEU is to be paid for until 2058.

Second and no less fundamental is the need for Member States to tackle so-called structural reforms - often internal reforms where EU jurisdiction does not reach, such as pensions or labour market reforms - which they have been promising for two decades in annual National Reform Plans, in the multi-level negotiating process called the European Semester. The problem is that, although the Structural Funds required the fulfilment of certain conditionalities linked to the Semester, in the best of cases these funds would only be a useful lever to carry out these reforms in the most benefited countries.

[Receive the most up-to-date analysis to your email or mobile through our Telegram channel]

That is why a €20 billion Structural Reform Programme had been proposed for the entire EU, regardless of income level (in its pilot phase three years earlier it had only 142), for the period 2021-2027. The response to COVID implied the possibility with the NGEU to replace this programme and multiply it exponentially. Thus, the Commission’s Communication notes that thanks to the MRR, the total number of Country-Specific Recommendations (reform proposals that the Commission makes annually to states) on which “some progress” has been made since 2020 has risen from 52% to 69%.This connects to the third dilemma: how to make the spending of European funds faster, more efficient and invested in agreed priorities at EU level. The EU’s main investment programme, the Structural Funds, used to be characterised by a very rigid – and multi-level, as much of the spending is managed by territorial administrations – system of multi-annual planning. Expenditure is only reimbursable to the Member State several years after implementation after a very rigorous evaluation of all documentation, and most expenditure must be co-financed by the Member State. Moreover, although evaluation has started to be done not only on the basis of the expenditure incurred but also on the basis of the results achieved, it is still under development. Therefore, the advent of the RRM meant trying something radically new, certainly on this gigantic scale, payment by results, but not linked to costs (Finance Not Linked to Costs) but to the achievement of targets linked to the structural reforms of the Semester committed to in each Recovery Plan. For example, at the end of 2022 an agreement was reached in extremis for labour reform, the urgency of which came about because it was a sine qua non condition for the disbursement of €12 billion of the MRR – and which were spent on projects that mostly have nothing to do with employment policies, something unthinkable in the traditional system.

The Commission’s communication thus states that by the end of 2023 no less than 1,150 milestones have been met by all member states. Certainly, delivering reforms in exchange for money has worked. However, if you look at the Operational Provisions of the Recovery Plan containing the milestones agreed with the Commission by Spain, you will see that they are very general: a milestone can be a result, a result can simply be that a law is passed and implemented. For example, the first Public Policy Evaluation Law was agreed in 2022 with no little haste as it was linked to the payment of one of the tranches of the MRR, and not to the creation – still pending and much needed – of a policy evaluation system in Spain, including that of European funds. The European Court of Auditors has repeatedly sounded the alarm on the major EU-wide weaknesses of such an incipient system, but one to which unprecedented amounts of funds have been allocated. Measuring results at the social level and linking them to concrete expenditure is not easy, especially at this scale.

However, the advantage for the long-suffering administrations is obvious, as management is simpler and the state receives the money in advance, unlike with the Structural Funds. The aforementioned mid-term evaluation of the RRF indicates that, although no evidence has been found of substitution of traditional 2014-2020 funds by the RRF, since it is already underway – and Spain is the furthest behind – it can already be seen that the 2021-2027 Structural Funds will only begin to be spent once it is no longer possible to do so through the Recovery Plan, which could mean that by 2026 – the last year of the RRF – there will be a huge bag of traditional funds to be spent, under the aforementioned N+3, until 2030.

And this, finally, is the ultimate dilemma of the Recovery Plan, being in fact a critique of the Structural Funds. Faster, easier to spend, more result-linked, but much more centralised, even in federal states like Germany, which is unprecedented. In principle the Recovery Plan runs out in 2026, as it was an extraordinary instrument outside the EU budget and financed by debt, although Commission President Von der Leyen – who will probably succeed herself this July – has already threatened to repeat the feat of agreeing the MRR with the Social Climate Fund – presented only two months after the historic NGEU agreement at the four-day summit in July 2020 – and which, after great resistance, will mean that the EU will have to pay the EU budget for the Recovery Plan in 2026, after great resistance, will mean that in 2026-2024 there will be a new €65 million fund (financed by revenues from emissions trading) to finance vulnerable households and the decarbonisation of transport.

Time in Brussels is relative, and while the focus is shifting to the June 2024 elections, in reality the post-2027 is already being thought about, as the Commission’s proposals for the new 2028-2034 budget will be made in May 2025, and will focus much of the political capital of the legislature. In all of this, how much of the MRR will remain after 2026 will be no minor issue, especially with regard to the future post-2027 Cohesion Policy, the first announcements of which have just been made by the High-Level Group led by Rodríguez-Pose. In this group, great emphasis is placed on the persistence of great territorial inequalities and the so-called “development traps” whereby many territories – in Spain there are many – are able to emerge from the lowest part of the GDP per capita table, but are then unable to become competitive territories at the European level, no matter how much EU money is transferred to them.

One of the questions is to what extent Cohesion Policy can be equipped with the new clothes of the RRM without distorting its territorial and multi-level essence – something in which the Recovery Plan suffers, as the Commission’s own Communication admits. As its accompanying study on the relationship between the RRM and the Structural Funds states, both funds finance the same things – and are managed by the same teams – but their intervention logic is different, and their management is highly centralised, as regional authorities have complained.

While it may still be premature to say that Cohesion policy simply needs to be transformed into a new Next Generation post-2027, the coming months will see a battle over what should be the dominant paradigm of the European budget in the coming decades: improvements to traditional funding or significant change, long-term investments versus responses to successive poly-crises, own-fund financing or pooled debt. The recent revision of the traditional budget with cuts to traditional policies to finance spending related to the new war climate, more borrowing, and funds for European technological sovereignty, suggests that while 2020 was a revolutionary year for EU finances, the COVID crisis was only the trigger for more radical changes for the Union of tomorrow.

Se puede leer el artículo original en español

ARTÍCULOS RELACIONADOS

ERIC VIDAL (REUTERS)

JOHANNA GERON (REUTERS)

Serafín Pazos-Vidal

Senior Expert, Rural and Territorial Development, European Association for Innovation in Local Development (AEIDL) e investigador

Analista de política europea con 20 años de experiencia en Bruselas, incluidos 15 como responsable de política europea de COSLA. Coordinador del Grupo de Expertos en Cohesión Territorial del CMRE (2008-2018) y miembro del Grupo de Expertos en Subsidiariedad del CdR. Autor de 'Subsidiarity and EU Multilevel Governance' (Routledge, 2019).

Etiquetas

Economía, cambio climático, UE, Unión Europea, Comisión Europea, Next Generation EU, España, Energía, Renovables, ucrania, coronavirus, Alemania, Países Bajos, impuestos Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 131 semanas

The EIB, a Public Bank for Europe’s Strategic Digital Transformation

Hace 132 semanas

The EU’s New Fiscal Rules

Lo más leído