Martes, 28 de julio de 2026

Reforming the Fiscal Rules: Is it possible to combine fiscal sustainability and investment?

MARAVILLAS DELGADO

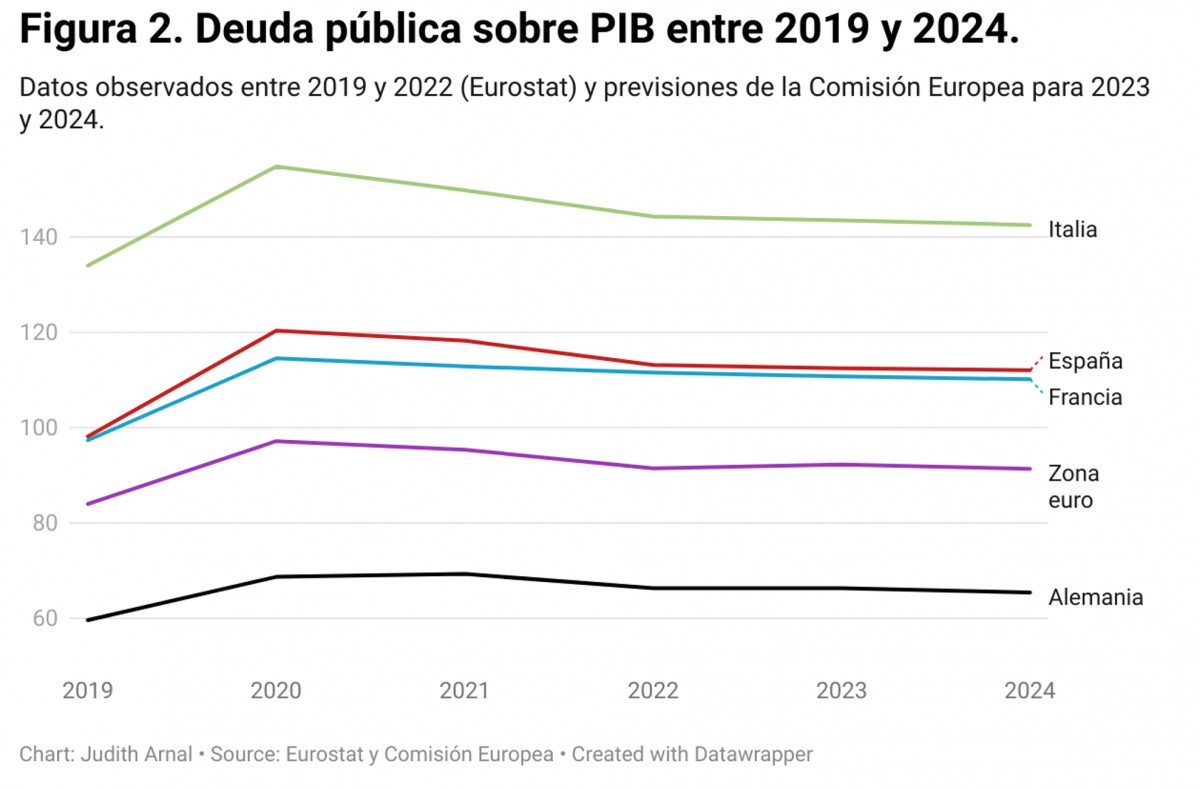

According to the European Commission’s economic forecasts, the EU and the euro area will have higher government deficit and debt levels in 2024 than in 2019. Government bond yields are also likely to be higher.When the general escape clause of the Stability and Growth Pact, activated in 2020 to accommodate the need for higher public spending to deal with the pandemic and the energy crisis, ceases to apply in 2024, EU Member States’ public deficit and debt levels are likely to be higher than at the end of 2019, as shown in Figures 1 and 2.

Figure 1.- Public deficit to GDP between 2019 and 2024

Figure 2.- Public debt to GDP between 2019 and 2024

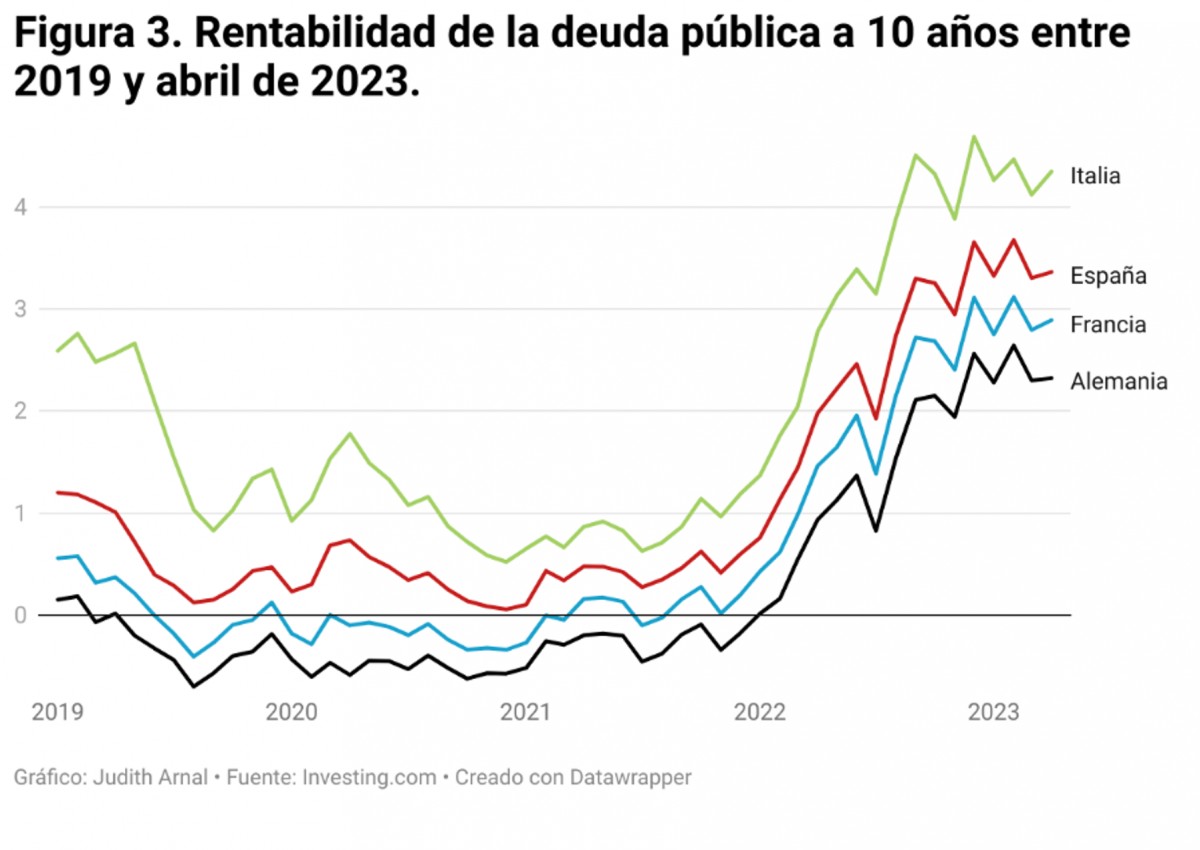

Government bond yields are also likely to be higher than in 2019, given both their recent evolution, shown in Figure 3, and the tightening of monetary policy, characterised not only by interest rate hikes but also by a progressive reduction of the European Central Bank’s balance sheet.

Figure 3.- 10-year government bond yields from 2019 to April 2023

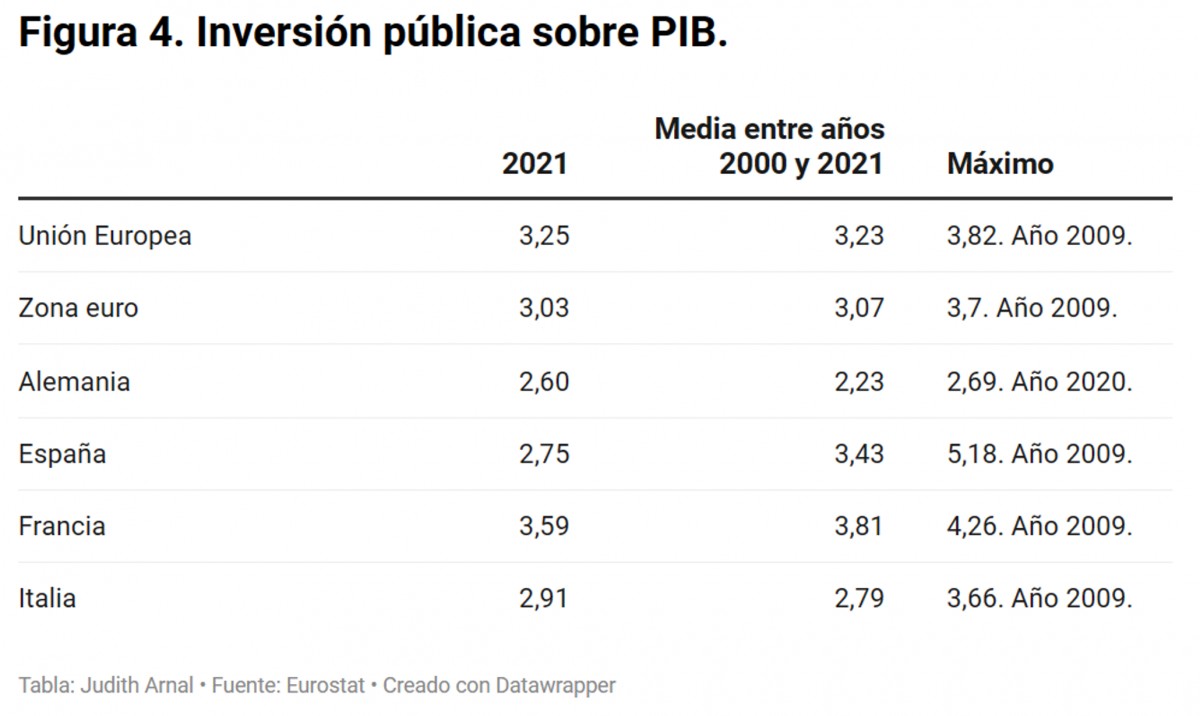

Investment needs will also be much higher.This worse fiscal position will also be accompanied by higher public investment needs, acting as a catalyst for private investment. As shown in Figure 4, in 2021, the EU and the euro area managed to recover average public investment levels between 2000 and 2021. But of the four large euro economies, two (France and Spain) failed to recover in 2021 the average level of investment between 2000 and 2021. And of course, all of them fell far short of the peak levels of public investment, which in most cases were observed in 2009, just before the onset of the euro area sovereign debt crisis.

Figure 4.- Public investment to GDP

The EU thus finds itself with lower levels of public investment than before the onset of the sovereign debt crisis, but it is more than likely to face historic investment needs: if the EU is to be competitive in an increasingly fragmented world on the basis of a sustainable growth model, it needs to invest heavily in green transition and digital transformation. At the same time, rising geopolitical tensions call for an increase in defence spending, not least to meet NATO’s 2% target. And of course, it should not be forgotten that the EU is likely to have to bear most of the costs of Ukraine’s reconstruction, which several international organisations have put at 380 billion euros. On top of all this, there will be growing current expenditure on pensions and health care, which will come with an increasingly ageing population.

And it should be borne in mind that national governments now have an extra source of public resources from the National Recovery Plans. But in 2026, if nothing changes, this source will no longer be available.

These elements make it urgent to reach an agreement to reform fiscal rules. But the question is: is there a possible reform of fiscal rules that would combine the sustainability of public finances with the need for huge investments?

The details of the European Commission’s proposal would maintain the sacrosanct reference figures of 3% of GDP for the public deficit and 60% of GDP for public debt.

The principle of simplicity is also reflected in the proposal by introducing nationally financed net primary public expenditure as the only operational indicator. The evolution of net government expenditure should ensure that the government debt-to-GDP ratio is on a plausible downward path for countries with a government debt-to-GDP ratio above 60%. This allows country-specific situations to be taken into account, replacing the current general and homogeneous rule of a reduction in the government debt ratio of 1/20 [1]. In the interests of greater simplicity, provisions that introduce excessive complexity, such as the significant deviation procedure or the matrix of fiscal adjustment requirements, are also eliminated.

The principle of flexibility is also included, with the possibility of extending the horizon of the structural fiscal adjustment plan from 4 to 7 years, provided that the Member State submits structural reforms and investments that support EU priorities in areas such as the ecological transition, digital transformation, security and defence. The escape clauses, both general and country-specific, are maintained, allowing for deviation from spending targets in case of a severe recession for the EU or the euro area as a whole or in case of exceptional circumstances beyond the reach of the Member State with a strong impact on its public finances.

To follow, for countries with a government debt-to-GDP ratio above 60% or a government deficit above 3%, the Commission will present its technical adjustment path, anchored on a government debt sustainability analysis. In preparing this path, net public expenditure may not grow faster than GDP over the medium-term horizon of the plan. For countries with a government debt below 60% and a government deficit below 3%, the Commission will not prepare a technical path, but will provide technical information to the Member State to ensure that the government deficit remains below 3% of GDP over the medium term.

Another safeguard mechanism means that if the government deficit is not below 3% of GDP, the Member State has to carry out a minimum annual adjustment of 0.5% of GDP. However, there is ambiguity in the Commission’s proposal as to the details of the above-mentioned 0.5% of GDP per year reduction.

Also, Member States with an extended horizon for the fiscal adjustment plan will have to ensure that the adjustment is not left to the final years, with the bulk of the adjustment concentrated in the first four years.

Finally, the decision on the activation of the general escape clause will be taken by the EU Council, on the basis of a recommendation from the European Commission.

Secondly, in the case of countries with challenges to debt sustainability that deviate from the fiscal path established in the medium-term budget plan, the Excessive Deficit Procedure will be opened by default. Thus, the opening of the Excessive Deficit Procedure for debt is facilitated, while the Excessive Deficit Procedure for non-compliance with the deficit criterion remains unchanged.

Third, financial penalties are reduced [2], thus facilitating their application in cases of deviations from the fiscal path set out in the structural fiscal plans.

Finally, non-compliance with the reform and investment commitments that motivated the extension of the deadline beyond 4 years could lead to a shortening of the adjustment period.

But really, beyond the details that can be ironed out in the technical and political negotiations in one direction or another, the main open question is how to combine sustainability and investment. And indeed, this has always been the debate, as the name of the Stability Pact (fiscal sustainability) and Growth (investment) shows.

This led to the reform of the Pact in 2005, with the aim of reinforcing the economic rationality of the rules by introducing the country-specific Medium-Term Budget Objective indicator, defined in terms of the structural balance.

However, the outbreak of the sovereign debt crisis again highlighted the failure of the Pact to prevent large fiscal imbalances, and a succession of tweaks to the rules followed: In 2011, the so-called "Six Pack" was adopted, introducing the expenditure benchmark in the preventive arm and the 1/20 rule on public debt reduction in the corrective arm; in 2012, the "Two Pack" was adopted, to strengthen control and surveillance in the euro area; in 2013, the "Fiscal Compact" led to member states having to anchor fiscal rules in their national legal systems.

The havoc wreaked by the sovereign debt crisis on public investment levels in the EU prompted the presentation in 2015 of new guidelines on the implementation of the Pact, in order to encourage investment and structural reforms and to take account of economic cycles.

And so we arrive at the current situation, in which a new reform of the fiscal rules is being considered. And it is important that this time we get it right and that the rules that are agreed are actually complied with. IMF research shows that non-compliance with fiscal rules has been behind the pro-cyclicality of fiscal policies.

It is therefore necessary to take the final step and introduce a permanent facility to finance public investments in key areas, such as the digital transformation and the green transition, while also playing a stabilisation role throughout the cycle. A first step would be to extend the application horizon of the Next Generation EU (NGEU) beyond 2026. The amount of NGEU funds spent so far is far below the projections made in 2020, so extending the deadline would only ensure that Member States actually invest the funds initially budgeted.

But it is necessary to go further and definitely constitute a permanent facility. The move towards a permanent facility for financing investments is not a question of lack of funds. By way of example, it suffices to refer to the European Stability Mechanism (ESM), an intergovernmental institution created by the eurozone countries, which played a key role in financial assistance programmes during the sovereign debt crisis, but which has been in hibernation for several years. The ESM has a capital paid up by eurozone member states of 80 billion euros, of which more than 9 billion euros corresponds to Spain. With the leverage that this paid-in capital allows, the ESM has a financial capacity of 500 billion euros, of which more than 400 billion euros are available. In other words, there is an institution in which the member states of the Eurozone have 80 billion euros paid up, which has a significant financial capacity, and yet it remains in a state of hibernation. This does not seem a reasonable situation, especially in light of the major challenges facing European countries.

In any case, it would be naïve to think that simply having more funds for public investment will solve the EU’s problems. It is clear that there are limits to the absorption capacity of public investment and this has been highlighted by the National Recovery Plans. It is therefore imperative that both the EU and Member States take appropriate administrative measures to ensure a faster channelling of public investment. Of course, measures to ensure the efficiency of public spending and the allocation of resources to the most efficient uses are also welcome.

Notwithstanding, the significant challenges facing the EU and the resulting strong investment needs mean that a reform of the fiscal rules will not be sufficient. If only fiscal rules are reformed, it will be difficult to combine fiscal sustainability and investment. Therefore, in addition to extending the horizon for the implementation of the NGEU, it is vital that a permanent facility to finance investment is finally introduced. It is not a problem of lack of resources. If the political will is there, it is possible. Let us hope that we do not have to face a new crisis in order to continue to make firm progress on the Economic and Monetary Union project.

[1]Under the current rules, the government debt-to-GDP ratio must be reduced annually by 1/20th of the difference between the government debt level and the 60% reference value.

[2]In the past, the high level of financial sanctions discouraged their application, as they could worsen the macroeconomic and fiscal situation of a country already in default.

And it should be borne in mind that national governments now have an extra source of public resources from the National Recovery Plans. But in 2026, if nothing changes, this source will no longer be available.

These elements make it urgent to reach an agreement to reform fiscal rules. But the question is: is there a possible reform of fiscal rules that would combine the sustainability of public finances with the need for huge investments?

The Commission has not had an easy job in formulating its proposal, as member states’ positions are very much at odds.After months of consultations with member state capitals, the European Commission published its proposal for reforming EU economic governance at the end of April, centred on the idea of ensuring the sustainability of public debt and promoting inclusive and sustainable growth, and based on the principles of national ownership, flexibility and simplicity, which should be to the liking of southern EU member states, but introducing safeguards and compliance and enforcement mechanisms, as a way to please Germany and the so-called Hanseatic League. The Commission did not have an easy job. The reform of the fiscal rules is an issue with very conflicting positions and where Germany and the Hanseatic League may be clearly tempted not to reach an agreement so that in early 2024 the old rules will have to be reinstated.

The details of the European Commission’s proposal would maintain the sacrosanct reference figures of 3% of GDP for the public deficit and 60% of GDP for public debt.

The European Commission’s proposal clearly reflects the principles of national ownership, simplicity and flexibility.In order to promote the principle of national ownership, Member States will be required to submit a 4-year fiscal structural adjustment plan outlining their fiscal targets, measures to address their macroeconomic imbalances, as well as their investment and reform agenda. These plans will be analysed by the European Commission and approved by the EU Council on the basis of common criteria.

The principle of simplicity is also reflected in the proposal by introducing nationally financed net primary public expenditure as the only operational indicator. The evolution of net government expenditure should ensure that the government debt-to-GDP ratio is on a plausible downward path for countries with a government debt-to-GDP ratio above 60%. This allows country-specific situations to be taken into account, replacing the current general and homogeneous rule of a reduction in the government debt ratio of 1/20 [1]. In the interests of greater simplicity, provisions that introduce excessive complexity, such as the significant deviation procedure or the matrix of fiscal adjustment requirements, are also eliminated.

The principle of flexibility is also included, with the possibility of extending the horizon of the structural fiscal adjustment plan from 4 to 7 years, provided that the Member State submits structural reforms and investments that support EU priorities in areas such as the ecological transition, digital transformation, security and defence. The escape clauses, both general and country-specific, are maintained, allowing for deviation from spending targets in case of a severe recession for the EU or the euro area as a whole or in case of exceptional circumstances beyond the reach of the Member State with a strong impact on its public finances.

But the above principles are accompanied by important safeguards.But the principles of national ownership, simplicity and flexibility are accompanied by important safeguards. To begin with, the fiscal adjustment plan should ensure that the government debt ratio ends up at a lower level than at the start and that the government deficit complies with the 3% of GDP rule for 10 years after the adjustment period (4-7 years) in a no-policy-change scenario.

To follow, for countries with a government debt-to-GDP ratio above 60% or a government deficit above 3%, the Commission will present its technical adjustment path, anchored on a government debt sustainability analysis. In preparing this path, net public expenditure may not grow faster than GDP over the medium-term horizon of the plan. For countries with a government debt below 60% and a government deficit below 3%, the Commission will not prepare a technical path, but will provide technical information to the Member State to ensure that the government deficit remains below 3% of GDP over the medium term.

Another safeguard mechanism means that if the government deficit is not below 3% of GDP, the Member State has to carry out a minimum annual adjustment of 0.5% of GDP. However, there is ambiguity in the Commission’s proposal as to the details of the above-mentioned 0.5% of GDP per year reduction.

Also, Member States with an extended horizon for the fiscal adjustment plan will have to ensure that the adjustment is not left to the final years, with the bulk of the adjustment concentrated in the first four years.

Finally, the decision on the activation of the general escape clause will be taken by the EU Council, on the basis of a recommendation from the European Commission.

The European Commission’s proposal also contains mechanisms to ensure compliance and enforcement.As regards mechanisms to ensure compliance and enforcement, a number of measures are also introduced. Firstly, Member States will have to submit annual analyses of the degree of compliance with their plans, which will facilitate monitoring by the European Commission. The role of the Independent Fiscal Institutions (the Airef in the case of Spain) will be strengthened and, for example, they will have to provide an assessment of compliance with the budgetary outcomes reported by the government in their annual report.

Secondly, in the case of countries with challenges to debt sustainability that deviate from the fiscal path established in the medium-term budget plan, the Excessive Deficit Procedure will be opened by default. Thus, the opening of the Excessive Deficit Procedure for debt is facilitated, while the Excessive Deficit Procedure for non-compliance with the deficit criterion remains unchanged.

Third, financial penalties are reduced [2], thus facilitating their application in cases of deviations from the fiscal path set out in the structural fiscal plans.

Finally, non-compliance with the reform and investment commitments that motivated the extension of the deadline beyond 4 years could lead to a shortening of the adjustment period.

Beyond the details of the Commission’s proposal to be refined at the technical and political level, the main open question is how to combine fiscal sustainability and investment.Doubts can be raised about the Commission’s proposal. By way of example: isn’t an annual adjustment of 0.5% of GDP pro-cyclical? What indicator does this 0.5% adjustment refer to? How will compliance with the structural fiscal adjustment plan be guaranteed when there is a change of government? What criteria will be used to decide to extend the horizon of the adjustment plan from 4 to 7 years? Is there really national ownership for states with a public debt ratio above 60% of GDP if the Commission presents technical adjustment paths?

But really, beyond the details that can be ironed out in the technical and political negotiations in one direction or another, the main open question is how to combine sustainability and investment. And indeed, this has always been the debate, as the name of the Stability Pact (fiscal sustainability) and Growth (investment) shows.

The main element in ensuring sustainability is that the fiscal rules that are agreed are actually implemented. And for that, they have to be realistic.The main element in ensuring sustainability is that the fiscal rules that are eventually agreed are actually implemented. And for that, they have to be realistic. There is no point in having very tough fiscal rules if, when the moment of truth arrives, exceptions are applied to avoid their implementation. And the truth is that in the case of fiscal rules, the exception has ended up becoming the rule, leading to successive reforms. Past deviations by some member states from sustainable fiscal paths have so far been penalised by financial markets, rather than having EU institutions play a preventive role to avoid having to reach financial stress.

[Recibe los análisis de más actualidad en tu correo electrónico o en tu teléfono a través de nuestro canal de Telegram]

Initially, the fiscal rules were very simple: the public deficit to GDP had to remain below 3%, public debt to GDP below 60% and medium-term fiscal positions had to be balanced or in surplus. But these rules led to pro-cyclical behaviour by some member states. Thus, in 2003, despite the fact that France and Germany exceeded the 3% of GDP government deficit benchmark, the EU Council decided to suspend the Excessive Deficit Procedure that had been opened for them, contrary to the European Commission’s Recommendation. Thus, the Commission decided to take the case to the CJEU, which nevertheless ruled in favour of the EU Council.This led to the reform of the Pact in 2005, with the aim of reinforcing the economic rationality of the rules by introducing the country-specific Medium-Term Budget Objective indicator, defined in terms of the structural balance.

However, the outbreak of the sovereign debt crisis again highlighted the failure of the Pact to prevent large fiscal imbalances, and a succession of tweaks to the rules followed: In 2011, the so-called "Six Pack" was adopted, introducing the expenditure benchmark in the preventive arm and the 1/20 rule on public debt reduction in the corrective arm; in 2012, the "Two Pack" was adopted, to strengthen control and surveillance in the euro area; in 2013, the "Fiscal Compact" led to member states having to anchor fiscal rules in their national legal systems.

The havoc wreaked by the sovereign debt crisis on public investment levels in the EU prompted the presentation in 2015 of new guidelines on the implementation of the Pact, in order to encourage investment and structural reforms and to take account of economic cycles.

And so we arrive at the current situation, in which a new reform of the fiscal rules is being considered. And it is important that this time we get it right and that the rules that are agreed are actually complied with. IMF research shows that non-compliance with fiscal rules has been behind the pro-cyclicality of fiscal policies.

Investment needs for the coming years are so enormous that a reform of fiscal rules alone will not be sufficient. It is necessary to introduce a centralised standing facility to finance investment and to increase administrative capacity to absorb that investment.Empirical evidence shows that the first thing governments cut when fiscal consolidation is necessary is investment spending, which is less perceptible to the electorate than cuts in current spending or tax increases. And in view of the huge public investment needs that the EU will have if it is to remain competitive and secure in today’s world, the tension between fiscal sustainability and investment needs will be stronger than ever. Incentives to invest that may be provided by fiscal rules, as possible golden rules, will not be sufficient for the large scale of investment that needs to be undertaken. Moreover, the European Commission’s proposal does not foresee any special treatment for any type of investment.

It is therefore necessary to take the final step and introduce a permanent facility to finance public investments in key areas, such as the digital transformation and the green transition, while also playing a stabilisation role throughout the cycle. A first step would be to extend the application horizon of the Next Generation EU (NGEU) beyond 2026. The amount of NGEU funds spent so far is far below the projections made in 2020, so extending the deadline would only ensure that Member States actually invest the funds initially budgeted.

But it is necessary to go further and definitely constitute a permanent facility. The move towards a permanent facility for financing investments is not a question of lack of funds. By way of example, it suffices to refer to the European Stability Mechanism (ESM), an intergovernmental institution created by the eurozone countries, which played a key role in financial assistance programmes during the sovereign debt crisis, but which has been in hibernation for several years. The ESM has a capital paid up by eurozone member states of 80 billion euros, of which more than 9 billion euros corresponds to Spain. With the leverage that this paid-in capital allows, the ESM has a financial capacity of 500 billion euros, of which more than 400 billion euros are available. In other words, there is an institution in which the member states of the Eurozone have 80 billion euros paid up, which has a significant financial capacity, and yet it remains in a state of hibernation. This does not seem a reasonable situation, especially in light of the major challenges facing European countries.

In any case, it would be naïve to think that simply having more funds for public investment will solve the EU’s problems. It is clear that there are limits to the absorption capacity of public investment and this has been highlighted by the National Recovery Plans. It is therefore imperative that both the EU and Member States take appropriate administrative measures to ensure a faster channelling of public investment. Of course, measures to ensure the efficiency of public spending and the allocation of resources to the most efficient uses are also welcome.

Conclusion.In short, reform of the fiscal rules is urgent. The EU cannot afford to start 2024 with the old rules. The European Commission’s proposal is a good basis for work, but what is crucial is that the final product to be agreed is realistic and compliance by Member States is ensured. We cannot return to episodes of the past, where the exception became the rule and fiscal rules were never fully implemented.

Notwithstanding, the significant challenges facing the EU and the resulting strong investment needs mean that a reform of the fiscal rules will not be sufficient. If only fiscal rules are reformed, it will be difficult to combine fiscal sustainability and investment. Therefore, in addition to extending the horizon for the implementation of the NGEU, it is vital that a permanent facility to finance investment is finally introduced. It is not a problem of lack of resources. If the political will is there, it is possible. Let us hope that we do not have to face a new crisis in order to continue to make firm progress on the Economic and Monetary Union project.

[1]Under the current rules, the government debt-to-GDP ratio must be reduced annually by 1/20th of the difference between the government debt level and the 60% reference value.

[2]In the past, the high level of financial sanctions discouraged their application, as they could worsen the macroeconomic and fiscal situation of a country already in default.

Se puede leer el artículo en español

ARTÍCULOS RELACIONADOS

Parlamento Europeo (Europa Press)

Judith Arnal

Doctora en Economía y técnico comercial y economista del Estado

Judith Arnal es consejera independiente del Banco de España y

miembro de su Comisión de Auditoría, investigadora sénior asociada

en el Real Instituto Elcano y miembro de su Consejo Científico, así

como profesora de economía y finanzas en la Universidad de Navarra

(Máster en Banca y Regulación Financiera) y en el Instituto de Empresa

(Master in Management).

Cuenta con una amplia experiencia profesional. Ha sido consejera del

Instituto de Crédito Oficial, de la empresa pública española encargada

de impulsar la Agenda Digital Red.es y de la empresa pública española

para la promoción de start-ups, ENISA. Trabajó durante 10 años en el

Tesoro Público español, llegando a ser directora del Gabinete Técnico

y de Análisis Financiero y a presidir la Comisión de Coordinación del

Sandbox Financiero, así como un Subcomité de la Autoridad

Macroprudencial española (AMCESFI). También ha sido directora de

Gabinete de la vicepresidenta primera y ministra de Economía y

Transformación Digital del Gobierno de España.

En el ámbito europeo, presidió durante más de tres años el Eurogroup

Working Group Task Force on Coordinated Action. Bajo su presidencia,

se prepararon los detalles técnicos de la reforma del Mecanismo

Europeo de Estabilidad (MEDE): el respaldo común al Fondo Único de

Resolución, la reforma de los programas de asistencia financiera

cautelar y la revisión del marco de sostenibilidad de la deuda. También

se trataron otros temas relativos a la Unión Bancaria, como la liquidez

en la resolución.

Doctora en Economía y Empresa por la Universidad de Navarra y

Técnico Comercial y Economista del Estado, ha sido galardonada con

varios premios, entre ellos el Premio Garrigues a la Mejor Abogada

Joven.

De nacionalidad española, Judith habla con fluidez inglés, francés,

alemán e italiano. Sus lenguas maternas son el español y el euskera.

Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 188 semanas

The Missing Debate in the Revision of the Fiscal Rules

Hace 231 semanas

Fiscal rules: national budgetary norms

Lo más leído