Martes, 28 de julio de 2026

The Unappealing Appeal of Spanish Banks

JAIME VILLANUEVA

On February 20th, the Spanish Treasury collected 637.1 million euros associated with the first instalment of the new tax on credit institutions developed by the Law 38/2022, of December 27. According to this Law, the tax has to be applied to those credit institutions which, in 2019, had raised total revenues from interests and fees above 800 million euros. Looking at the bank accounts published by the Spanish Banking Association (AEB), the Association of Savings Banks (CECA), and the National Union of Credit Cooperatives (UNACC), currently there are 9 institutions fulfilling this criteria: Santander, BBVA, Sabadell, Bankinter, Caixabank, Kutxabank, Abanca, Unicaja e Ibercaja. These banks should pay, in 2023 and 2024, 4.8% of the interest and fee margins earned the previous years (2022 and 2023, respectively). The first installment of 50% of this tax already collected in February tells us that the fiscal revenues for this year will be 1.2 billion euros. For next year the Treasury expects a similar figure.

Several of the affected credit institutions, together with the AEB and the CECA, have appealed to the High Court against this windfall tax. The objective of this article is to review what the data has to say about how appealing the arguments on each side are.

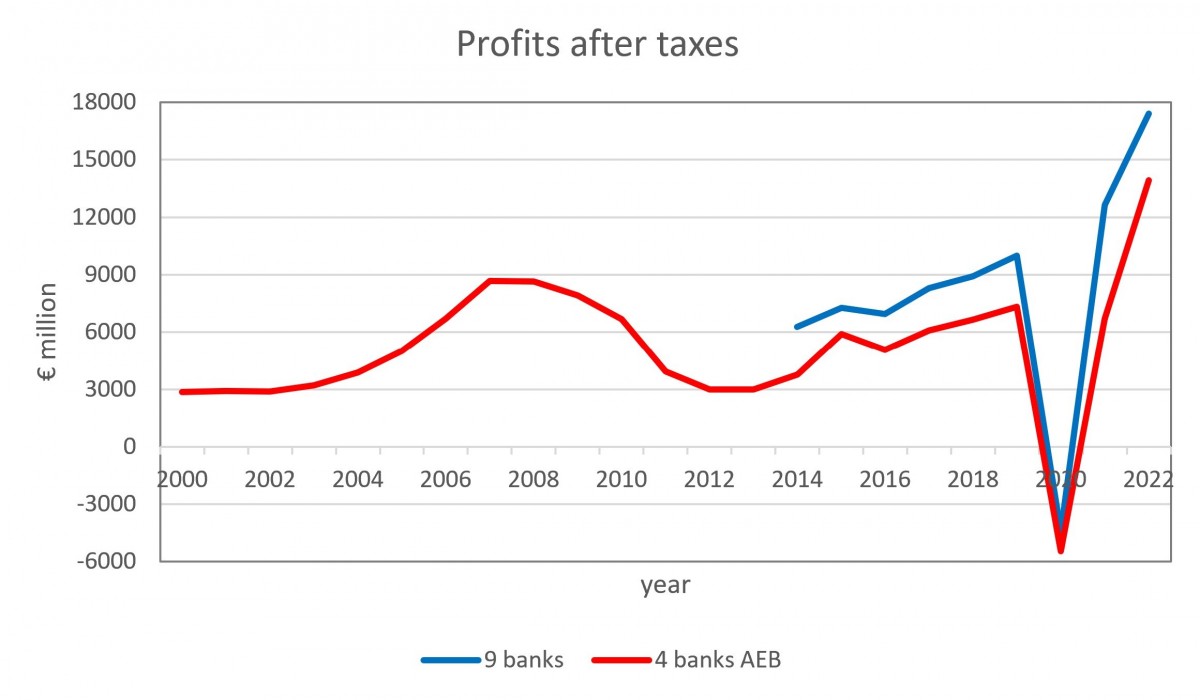

On the other hand, the preamble of the Law 38/2022, also includes banks as one of the sectors in the economy benefited by the current price hike in the sense that this general price increase generates windfalls which could be taxed temporarily. The following figure shows the profits after tax of these 9 companies (blue line) together with the corresponding data for the 4 banks (Santander, BBVA, Sabadell and Bankinter) which are members of the AEB and for which there is more data available. According to the public financial statements of these companies, their joint profits after tax were 17.4 billion euros. This is twice the average profits of these banks between 2014 and 2021, excluding 2022, the pandemic year in which they had losses overall. If we concentrate in the 4 banks in the AEB, their combined profits in 2022 were 1.6 times larger than their combined profits in 2007, the year between 2000 and 2021 where they earned more money.

Banks, on the other hand, present a number of arguments. One has to do with the potential negative impact on competition since the tax is levied on some institutions and not on all of them. With respect competition, we should not forget that these 9 banks represent, approximately, 82% of all assets of this sector in Spain. It is hard to think how a tax of 4.8% applied for only 2 years to windfalls could have a significant effect on the degree of competition, or lack of it, in a sector with such overwhelming concentration.

A second argument maintains that the banking sector in Spain already pays a huge amount in taxes, proportionally larger than other sectors and banks in other countries. This argument regularly refers to a report by PwC about the tax contribution of the main banking groups in Spain during 2021. The report quantifies the tax effort of these banks, adding together everything they pay to the Estate, in the neighbourhood of 50% of profits before taxes, ratio that could increase to 60% if the new tax is included. This would place Spain in the first position within Europe regarding the tax contribution of the banking sector (it was second until now).

However, when one reads the report in more detail, there are several methodological issues worth remarking. First, the report only includes four countries when comparing Spain with Europe: Germany, France, Italy and the Netherlands. Second, the comparison between countries is not done with real data but with a theoretical tax model applied to a 'typical' bank. Third, the two main drivers of the tax contribution of banks in Spain are the Social Security payments and the VAT not recovered since financial services are exempted of paying the tax on value added. In Spain, one of the reasons the contributions to Social Security of the banking sector are larger than the rest of sectors is that average wages are the highest of all sectors and these contributions are proportional to salaries. On the other hand, the VAT exemption of financial services is a feature of the whole European Union. However, two (Germany and France) of the four countries involved in the comparison have lower VAT taxes than Spain and only one has it marginally higher (Italy). Thus, this also contributes to the larger tax effort of banks in Spain as compared to these other countries but it says noting with respect other countries with much larger VATs such as Denmark, Finland, Hungary or Croatia.

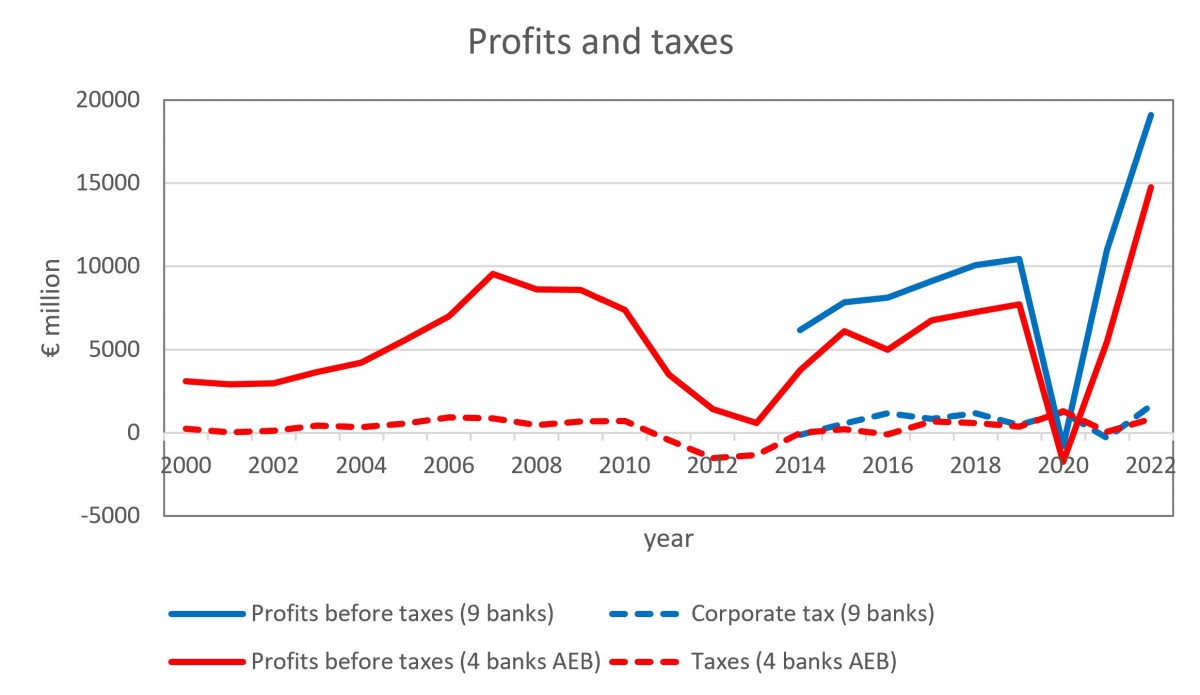

On the issue of how much taxes banks pay in Spain, we can look at the real data based on the public information they provide in their financial statements. The following figure plots profits before taxes (solid lines) of the 9 banks involved in the windfall tax (blue line) as well as those of the 4 banks in the AEB (red line) together with the corporate taxes (dotted lines) they have paid for the years between 2000 and 2022. In the 9 years for which there is data on these 9 banks, 2014 until 2022, these credit institutions have obtained a total profit before taxes of 81 billion euros. In those years, according to the same income and expenditure accounts, they have paid 6.6 billion euros. This implies an average effective corporate tax rate of 8.1%, much lower than the rate applicable to the banking sector of 30%. If we do the same computation for the 23 years we have data for the 4 banks in AEB, the corresponding effective average corporate tax rate is even lower, 4.7%.

Finally, there is another issue worth mentioning but somehow hidden from plain view. Since last summer, the Eurosystem has decided to raise interest rates in the largest hike in the history of the euro. The problem with this increase is that it will generate losses in most of central banks within the Eurosystem (ECB included) for the coming years. The reason is twofold. On the asset side, return is anchored to low rates associated with public debt and the different rounds of cheap TLTROs the Eurosystem conducted to navigate the financial crisis first and the consequences of the Covid pandemic later. On the liability side, the cost of central bank deposits increases with the policy rates. These losses of central banks mean a corresponding transfer of resources to credit institutions since they are not paying the rate they should be paying for the funds they borrow from the central bank but are earning a higher rate for their deposits there. These losses also mean the Treasuries in the euro area will not receive the seigniorage revenues they used to have. The governor of the Bank of Spain, Pablo Hernández de Cos, has already announced that his institution will have losses in the near future. Thus, the Spanish Treasury will not receive its corresponding share of the seigniorage which amounts to about 2 billion euro per year in the following years.

This is the data. It does not make the appeals of the Spanish banks to the High Court very appealing from an economic point of view but the conclusions are all yours.

Several of the affected credit institutions, together with the AEB and the CECA, have appealed to the High Court against this windfall tax. The objective of this article is to review what the data has to say about how appealing the arguments on each side are.

[Recibe los análisis de más actualidad en tu correo electrónico o en tu teléfono a través de nuestro canal de Telegram]

On the side of the Spanish Government, the preamble of the law specifies that 'in the recent past, an important amount of public resources was directed towards the bailing out of several financial institutions.' Although this fiscal effort was first announced as a line of credit with no impact whatsoever in the public deficit and with no cost to the citizens, at the end it turned out being a formal rescue package with conditioning. This rescue has already accumulated, according to the last report of the Bank of Spain from November 20, 2019, 65.7 billion euros in losses of public resources that will never be recovered. These funds were directed towards the restructuring and recapitalisation of credit institutions that later on were merged with or bought by the very same banks now are paying the windfall tax. Of these funds, almost 20.6 billion were used to institutions later included in CaixaBank group, 15.6 billion were spent in banks now in the BBVA group, 12.7 billion in banks merged with Banco Sabadell, 9.2 billion were directed towards Abanca, 5.1 billion to Unicaja and 392 million to Kutxabank.On the other hand, the preamble of the Law 38/2022, also includes banks as one of the sectors in the economy benefited by the current price hike in the sense that this general price increase generates windfalls which could be taxed temporarily. The following figure shows the profits after tax of these 9 companies (blue line) together with the corresponding data for the 4 banks (Santander, BBVA, Sabadell and Bankinter) which are members of the AEB and for which there is more data available. According to the public financial statements of these companies, their joint profits after tax were 17.4 billion euros. This is twice the average profits of these banks between 2014 and 2021, excluding 2022, the pandemic year in which they had losses overall. If we concentrate in the 4 banks in the AEB, their combined profits in 2022 were 1.6 times larger than their combined profits in 2007, the year between 2000 and 2021 where they earned more money.

Banks, on the other hand, present a number of arguments. One has to do with the potential negative impact on competition since the tax is levied on some institutions and not on all of them. With respect competition, we should not forget that these 9 banks represent, approximately, 82% of all assets of this sector in Spain. It is hard to think how a tax of 4.8% applied for only 2 years to windfalls could have a significant effect on the degree of competition, or lack of it, in a sector with such overwhelming concentration.

A second argument maintains that the banking sector in Spain already pays a huge amount in taxes, proportionally larger than other sectors and banks in other countries. This argument regularly refers to a report by PwC about the tax contribution of the main banking groups in Spain during 2021. The report quantifies the tax effort of these banks, adding together everything they pay to the Estate, in the neighbourhood of 50% of profits before taxes, ratio that could increase to 60% if the new tax is included. This would place Spain in the first position within Europe regarding the tax contribution of the banking sector (it was second until now).

However, when one reads the report in more detail, there are several methodological issues worth remarking. First, the report only includes four countries when comparing Spain with Europe: Germany, France, Italy and the Netherlands. Second, the comparison between countries is not done with real data but with a theoretical tax model applied to a 'typical' bank. Third, the two main drivers of the tax contribution of banks in Spain are the Social Security payments and the VAT not recovered since financial services are exempted of paying the tax on value added. In Spain, one of the reasons the contributions to Social Security of the banking sector are larger than the rest of sectors is that average wages are the highest of all sectors and these contributions are proportional to salaries. On the other hand, the VAT exemption of financial services is a feature of the whole European Union. However, two (Germany and France) of the four countries involved in the comparison have lower VAT taxes than Spain and only one has it marginally higher (Italy). Thus, this also contributes to the larger tax effort of banks in Spain as compared to these other countries but it says noting with respect other countries with much larger VATs such as Denmark, Finland, Hungary or Croatia.

On the issue of how much taxes banks pay in Spain, we can look at the real data based on the public information they provide in their financial statements. The following figure plots profits before taxes (solid lines) of the 9 banks involved in the windfall tax (blue line) as well as those of the 4 banks in the AEB (red line) together with the corporate taxes (dotted lines) they have paid for the years between 2000 and 2022. In the 9 years for which there is data on these 9 banks, 2014 until 2022, these credit institutions have obtained a total profit before taxes of 81 billion euros. In those years, according to the same income and expenditure accounts, they have paid 6.6 billion euros. This implies an average effective corporate tax rate of 8.1%, much lower than the rate applicable to the banking sector of 30%. If we do the same computation for the 23 years we have data for the 4 banks in AEB, the corresponding effective average corporate tax rate is even lower, 4.7%.

Finally, there is another issue worth mentioning but somehow hidden from plain view. Since last summer, the Eurosystem has decided to raise interest rates in the largest hike in the history of the euro. The problem with this increase is that it will generate losses in most of central banks within the Eurosystem (ECB included) for the coming years. The reason is twofold. On the asset side, return is anchored to low rates associated with public debt and the different rounds of cheap TLTROs the Eurosystem conducted to navigate the financial crisis first and the consequences of the Covid pandemic later. On the liability side, the cost of central bank deposits increases with the policy rates. These losses of central banks mean a corresponding transfer of resources to credit institutions since they are not paying the rate they should be paying for the funds they borrow from the central bank but are earning a higher rate for their deposits there. These losses also mean the Treasuries in the euro area will not receive the seigniorage revenues they used to have. The governor of the Bank of Spain, Pablo Hernández de Cos, has already announced that his institution will have losses in the near future. Thus, the Spanish Treasury will not receive its corresponding share of the seigniorage which amounts to about 2 billion euro per year in the following years.

This is the data. It does not make the appeals of the Spanish banks to the High Court very appealing from an economic point of view but the conclusions are all yours.

Hugo Rodríguez Mendizábal

Científico en el Instituto de Análisis Económico (CSIC)

También es investigador en MOVE y profesor afiliado de la Barcelona School of Economics. Sus áreas de investigación son la macroeconomía y la economía monetaria.

Ahora en portada

27 de julio de 2026

27 de julio de 2026

Noticias relacionadas

Hace 181 semanas

The Apocalypse Has Not Arrived to Spain Yet

Hace 210 semanas

From Covid-19 to the cost-of-living crisis: Poor social protection is Spain's Achilles heel

Lo más leído